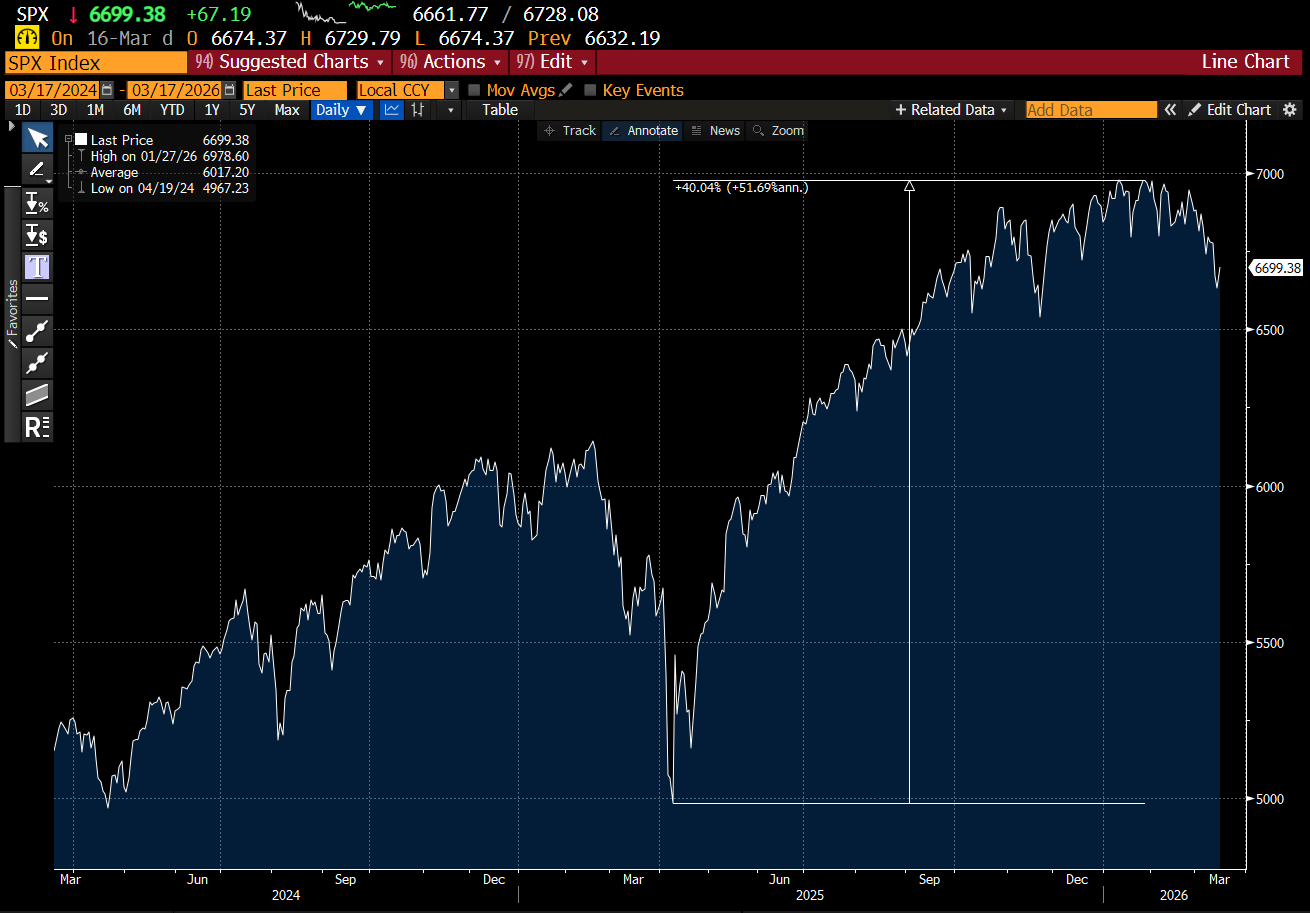

President Trump is the first “social media” president. You can see it in how he looks to not only dominate the social media narrative, but remains heavily influenced by it. If a policy gives good traction on social media, you should expect him to run with it. But ultimately, all his policies seem to be advancing an “America First” agenda. The Liberation Tariff day sell off was all about giving Trump leverage over US trade partners - which he largely achieved. Selling markets on the “Dump Trump” theme then was a disaster, as markets surged 40%.

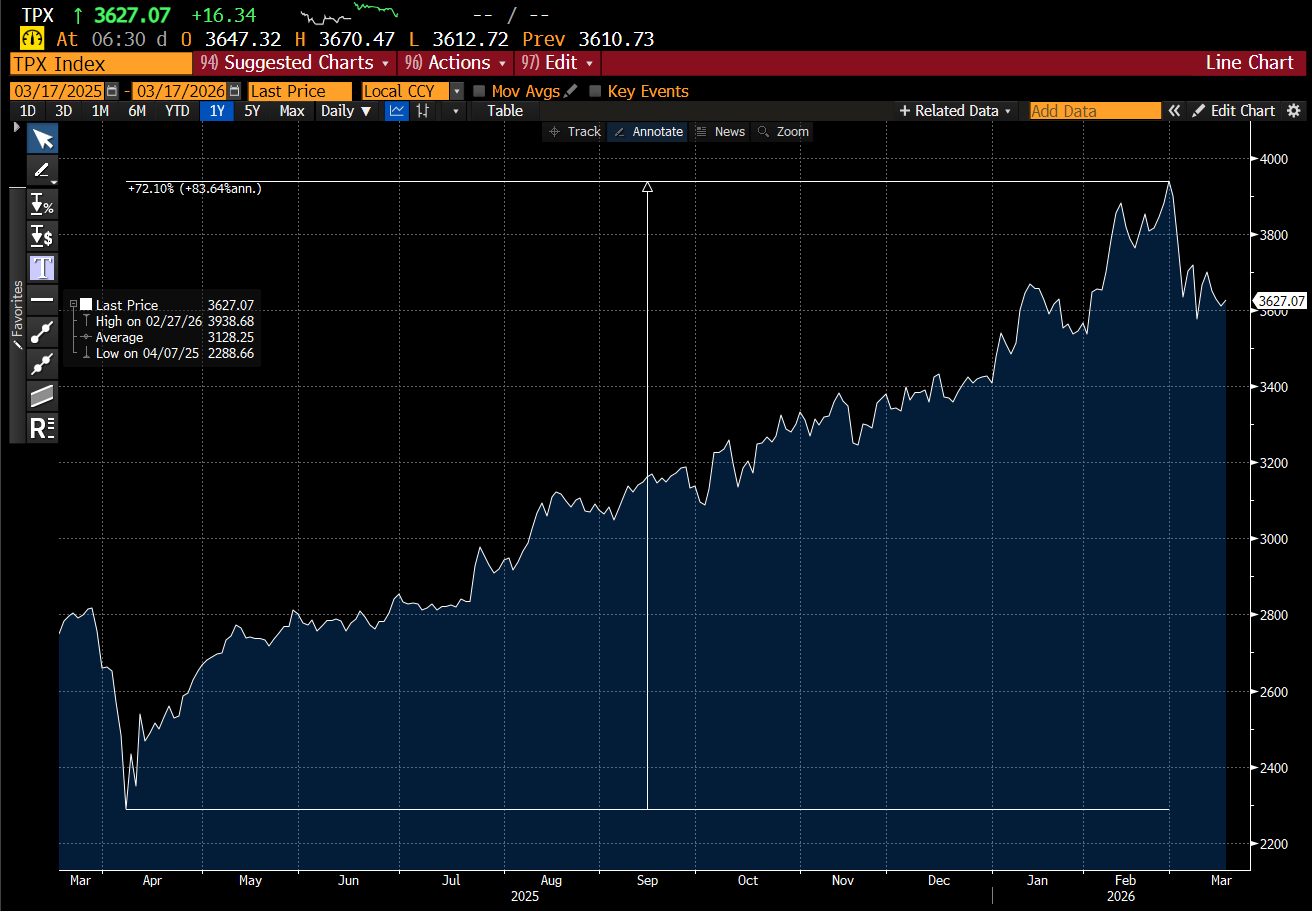

A better trade was to trade the reaction of allies who understood there was no alternative but to push the fiscal spend button. I liked Japan for this reason, which has been good until this month. Up 70% from the lows.

Even when you think Trump has decisively turned against someone - as he did with Elon Musk in 2025, Tesla has been a bad short. This is even with 2026 EPS forecast falling from USD 8 to USD 2 - the stock has held up. I hope I have mentioned that short selling is not for the overly logical or faint of heart (there is a decent argument that short selling is for no one).

Given this history - lets start from a “Smart Trump” assumption, and work from there. First of all, getting rid of an Iranian nuclear weapon program is an admirable objective. Various agreements to stop nuclear proliferation have obviously failed with India, Pakistan and North Korea all now in possession of nuclear weapons. And given the weakness of Iranian proxies, and Russia being tied down in Ukraine, if you were going to wage war on Iran if not now when?

The “Dumb Trump” argument here was that that there is a risk that this turns into a quagmire - but perhaps that suits the US. I can see three reasons this would be the case.

Firstly, if the rest of the Middle East is pulled into conflict, this would make the whole area an unreliable partner for fossil fuel, which would suit US producers, who would be poised to take market share.

Secondly, a prolonged war would likely pull China into the Middle East. For all their build out of military might, no one has actually seen the Chinese military actually do anything for nearly 50 years. Can the Chinese navy secure oil supply? And if the Chinese navy is pinned in the Middle East, would they also have the capability to attack Taiwan? You can see how this would be a positive for US policy makers.

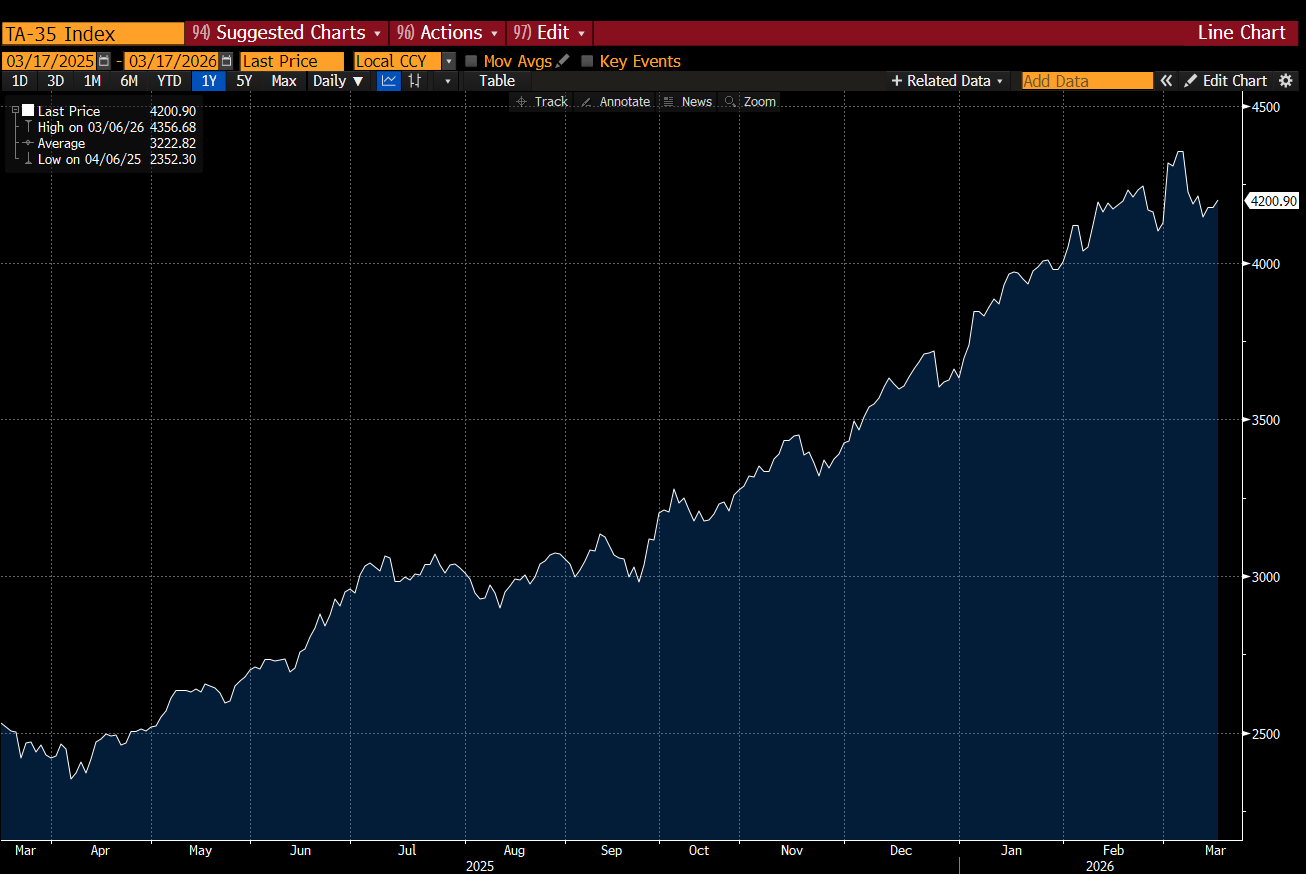

And finally, it enhances US leverage over its trade partners. If Europe and Asia build up their own military, it is US interest to replace military reliance with energy reliance. In other words, the War in Iran actually helps Trump advance an America First agenda. As pointed out before, if the War in Iran was really going wrong, I would not expect Israeli shares and currency to be doing so well. The stock market is near all time highs.

And Israeli Shekel is strong, even what has been a conspicuously strong dollar environment. Down is strengthening here - i.e. you need less Shekels to buy a US dollar.

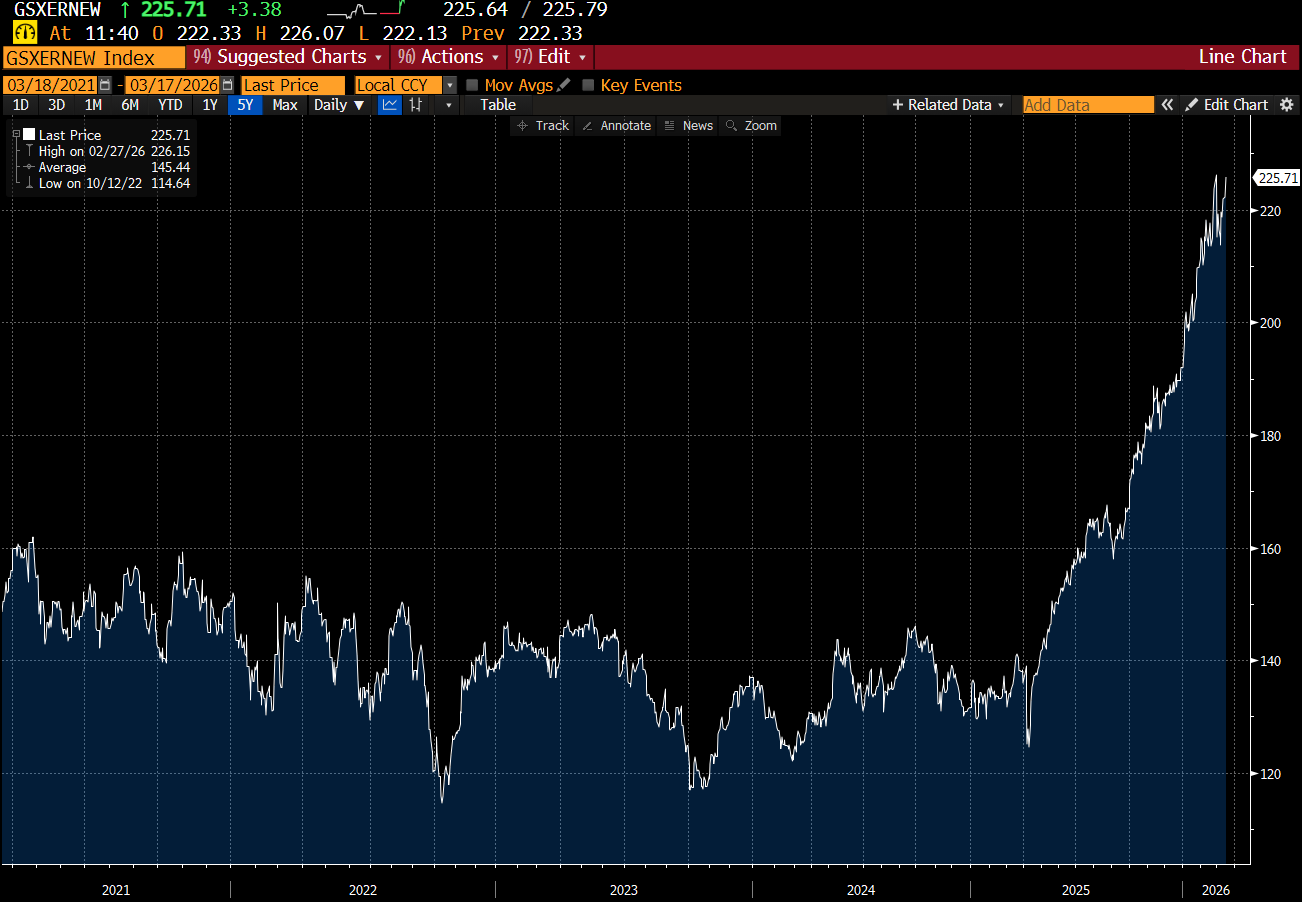

What does this mean? Perhaps a quagmire actually suits Trump - as far as an America First agenda concerned. This will give the US more power over energy markets ultimately, while making the Middle East a Chinese problem. If we assume this is the case (and I think we should until more information comes forward), then what is the reaction? As I have mentioned many times, I prefer trading the reaction rather than the action, as its tends to be safer. Chasing oil prices here risk all sorts of losses. The most obvious reaction is that European and Asian nations will realise that the US is trying to create leverage in the energy markets, to replace the defence and trade leverage that Trump has used up. The most obvious options for Europe and Japan are to beef up domestic energy sources. Market is ahead of me on this one - with the GS EU Renewable Index at all time highs, and doubled over the last year. The strength of this index this month is conspicuous.

That being said, I do wonder if wind energy stocks that have been pummelled by Trump’s anti renewable energy policies might be worth a look. Orsted is one stock that comes to mind. It had lost 85% of its peak value.

As a policy agenda, reducing reliance on energy suppliers such as Russia and Iran is not really a bad agenda. The problem is that is totally feasible for the US, but less so for its allies. But as the market shows, policy makers in Europe are at least aware of this.

So what am I thinking? Well there are two stages to a crisis. The first stage is when things are going wrong, but you don’t know they are going wrong. And the second stage is when you know they have gone wrong, and are now trying to fix. The crisis for Europe and Japan was phasing out of nuclear power without having a suitable replacement at hand. But judging by the performance of nuclear power stocks - governments and companies know this. One stock I owned from 2006 to late 2007 was a company called Doosan Infracore - now Doosan Enerbility (yes - I also don’t know how they choose these English names). What I loved about this stock is that one of its key business lines is to refurbish old nuclear power plants. The stock price tells you business is good. Is it still a buy? No idea - but you should be aware that shares outstanding has increased 4 fold since 2006, and revenue is flat from that period - so you are not getting a bargain…. and its Korean.

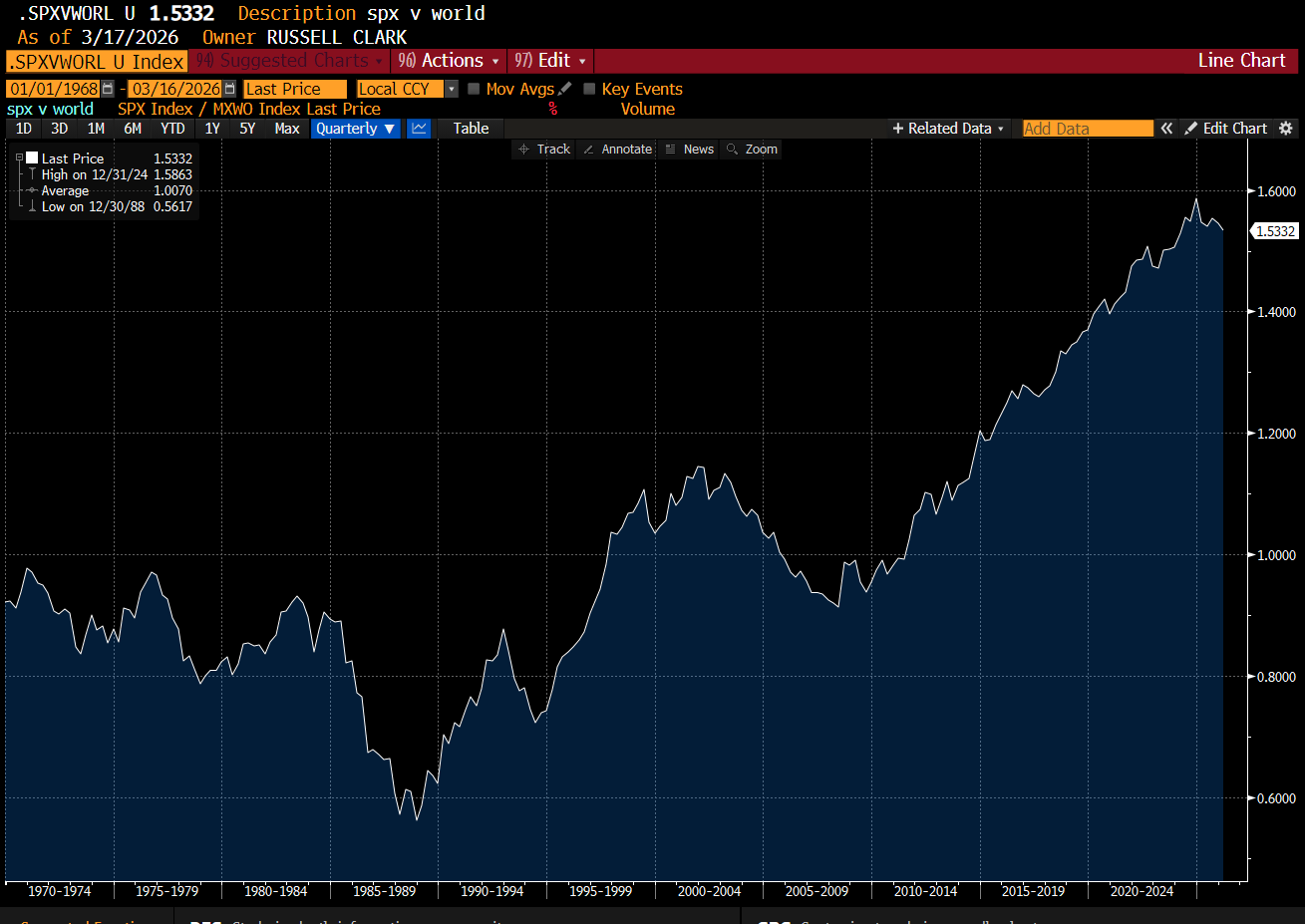

So what am I seeing and thinking? The War in Iran, like the Liberation Day tariffs, are meant to shock US allies out of the reliance on the old world order - reliance on the UN and treaties. This system no longer works for the US, and the US is trying to get their allies to free themselves from this system too. My best guess is that this will be successful, and markets are indicating this. I put the chances of recession very low - governments will spend whatever it takes. I see the cost of capital still rising - and I see Europe and Japan reforming. The market has been signalling a long Rest of the World versus the US for a year and a bit now. The War In Iran has shaken that up a bit - but it still looks valid to me.

On the longer time frame its still seems to have miles to run.

If I make the argument that Europe and Japan are at a turning point to my American and Israeli friends, they generally like to list all the reasons these nations are useless. But knowing you are useless is what happens at turning points. I think Europe and Japan still look okay to me - and strangely this is what Trump wants, in so far his agenda is to break apart a multilateral world, and encourage Western Allies to adopt their own Europe First and Japan First agendas. For fans of history, I am reminded of Admiral Perry and his Black Ships (Kurofune) who forced political change on Japan. They arrived in 1853, and from a starting point of a feudal society, a furious pace of industrial change was ushered into Japan. So much so that a mere 50 years later Japan beat Russia in a major war and secured control of Korea and Manchuria. Politically and more importantly in the equity market, I see a similar change underway. Rather than Admiral Perry and his Black Ships, perhaps we should talk of President Trump and his Orange Wave.