HOW COMPETITION WITH CHINA HAS CHANGED THE US

Politics, more than markets, seems to explains markets better these days

For years I believed that capital flows were the main drivers of asset markets (hence the title of the website), but I am starting to believe that free markets and capital flows were part of a larger political system, that is now being challenged and rewritten.

To explain this fully, we need some more context for the political/economic system that we have been in for the last 40 years or so. In the post World War II period from 1945 to 1970s, the focus of global economic policy was to have rising wages. This was in part driven by the ideological confrontation between the US and the USSR. It was politically important for the US to show that capitalism could also generate positive outcomes for workers, to reduce the appeal of communism. This is most clearly seen in the US Federal minimum wage, which rose 1000% from 1939 to 1979.

But by the 1970s the rise of the USSR was already been challenged and reversed. Politically, China has broken with Soviet Union, and opened diplomatic relations with the US. Economically, the US left the gold standard, and free market policies were beginning to be implemented. Just as rising minimum wages were a sign of the times, stagnant minimum wages since then have also been a sign of the times. Federal minimum wages have barely doubled in the US since 1980.

Politically, a free trade system suited the US. As by far the largest single importing nation, free trade institutions would naturally be influenced by US policy. Even in the hey day of Japanese growth, imports by Japan were only ever a fraction of the US. Free trade also offered a very appealing ideology, as the US not only sought the best possible life for Americans, but for all its trade partners. Globalisation and free trade was a policy that was meant to lift all boats.

However, the US is now seemingly regretting lifting the Chinese boat through free trade. The most likely reason for this is that China is now as large an importer as the US, meaning that free trade no longer gives the US natural political hegemony.

If we interpret “America First” policy as the US always being the largest economy in the world, this naturally turns American policy from free trade and all boats rising, to one of deliberating holding back of Chinese growth. As can also be seen below, the US can no longer “afford” a recession, as it would likely drop American GDP below Chinese GDP.

A political analysis of the US explains most American policy. The US needs to grow rapidly, and a bull market is necessary for this.. In simple terms, if rising returns to labour drove economic growth in the post World War II period, rising returns to capital has driven economic growth since the 1980s. US policy has moved from a panglossian free trade dogma of the 1980s (think the optimism of Reagan) to a “China must fail” thinking of Trump and Biden. Even the Anti-USSR rhetoric of the 1980s was enlivened with the ideal of allowing the supressed citizens of the Eastern Bloc to be free to do as they choose. A very tangible aspect of this “China must fail” mindset is the number of student visas the US has issued to Chinese students.

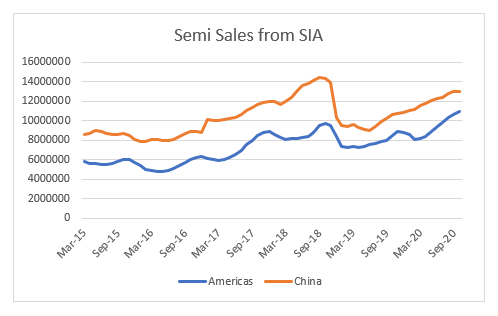

China has built up a substantial lead in 5G telecommunication technology. Regulatory and political attacks on the Chinese semiconductor industry led to a slow down in sales of semiconductors in China. However sales are now picking up again.

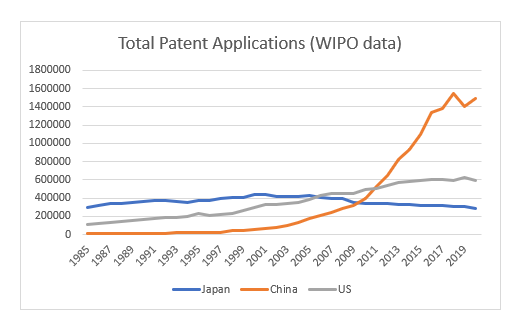

Despite the reduction in student visas for Chinese students, and the attack on Chinese semiconductor industry, China was one of the few nations to see patent applications rise in 2020.

However, US political action to slow China has led to a political reaction in China. In contrast to the US, China has made a concerted effort to enforce anti-trust laws in the tech space. Leading Chinese technology company Alibaba has seen is share prices collapse below their 2018 levels, while Google has tripled from 2018.

My take on this, is that in a ironic twist, the Chinese Communist Party realises that it needs to prove that it’s economic system works for everyone, not just the rich. Hence the much heavier regulation of the tech and property sector. The implication of such a policy change is profound. At its core is an attempt to move more of the spoils of economic growth to workers from capital owners, and means many policies will be contrary to the west. They include much more stringent antitrust regulation, the allowing of more bankruptcies, and raising the cost of capital to reduce property speculation, as well as running a strong currency policy to maximise real wages. For the West, this means that China will become a source of inflation rather than deflation. US consumers seem to recognise this reality, even if policy makers do not.

The biggest problem from investors and policymakers is that US policy implies that the West needs to act to stop average Chinese person from realising their full potential, which is a stark change from the policy of the last 40 years. Chinese policy remains one of free trade, and seeking to make it and its trade partners wealthier. The experience of the post World War II period is that trying to lift all boats is a winning policy, and yet markets are pricing in the opposite outcome. Its hard not to feel we are a generational turning point in many asset classes.

Really interesting take on the comparative landscape, vis a vis China and US. I just finished reading "2034" which provides a frightening hypothetical scenario if this clash of titans continues, especially in the political arena

Excellent article and a good continuation of your last post. However I’m not sure what you mean when you say this; “The experience of the post World War II period is that trying to lift all boats is a winning policy, and yet markets are pricing in the opposite outcome.” What are you alluding to that markets pricing in? Inflation, mega cap Tech continuing to win, supply chain beneficiaries also winning?