Since I first came up with the GLD/TLT trade, its having its first meaningful drawdown. To be fair, it has been on a blistering run.

The idea behind GLD/TLT was that we are in a rising cost of capital world, not because things are bad, but conversely because things are good. Governments are focused on demand management, full employment and rising wages. This means “systemic” inflation will be much higher going forward, UNLESS central banks stop being the natural born losers they have become in recent years and raise interest rates to keep asset prices in check. In 2022 central banks grew a pair, and declining asset prices checked rising inflation, but since then they have returned to type and have been desperate to cut interest rates. Intellectually, central banks are trapped in a world that no longer exists, but politically they are on the hook for the inflation that current policy settings are producing.

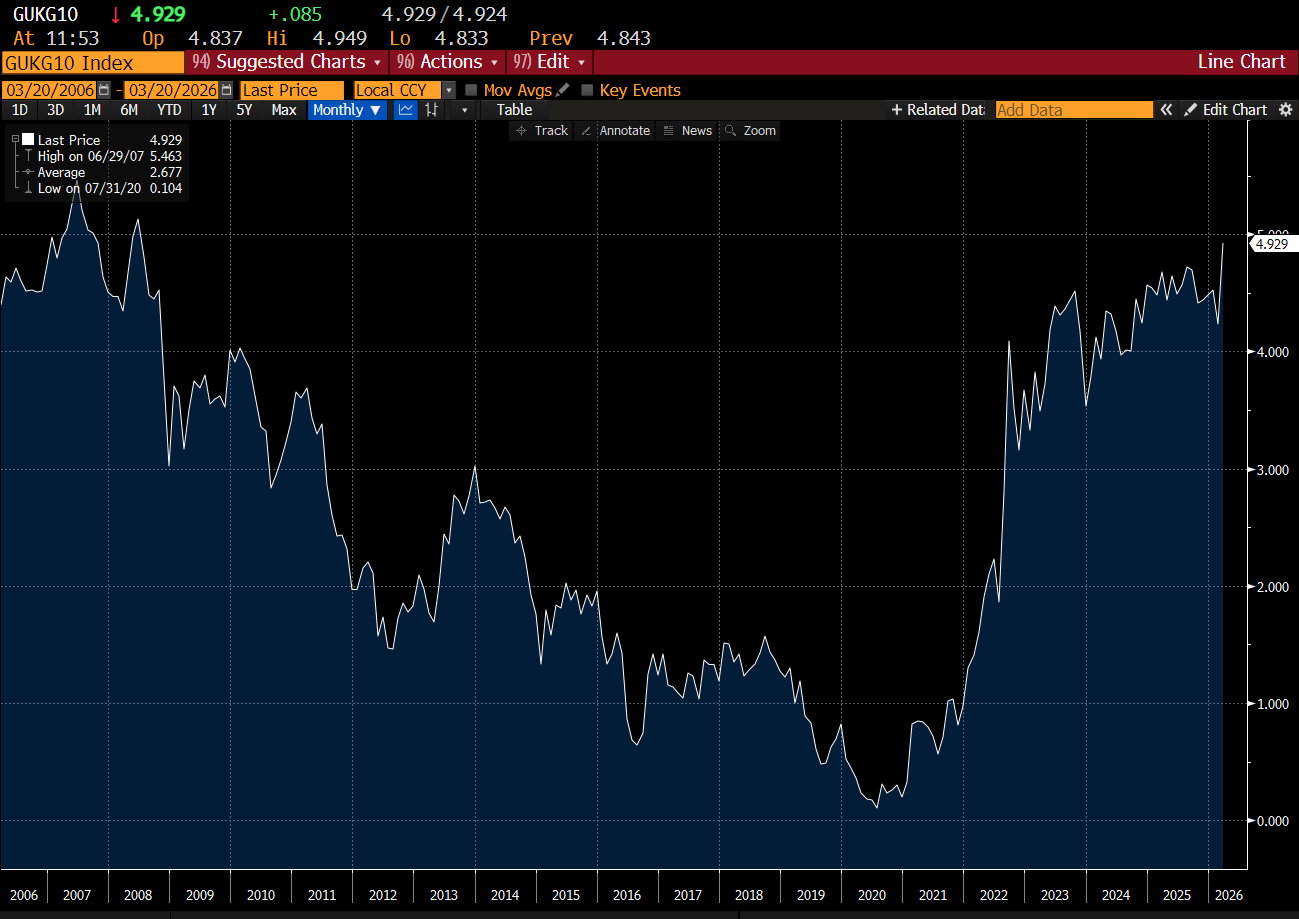

The market has been clearly telling them that the world has changed. 30 Year JGBs have continually sold off.

But central bankers, like many fund managers, are very keen on backtesting. That is they only want to do what worked in the past, so are reluctant to raise interest rates. The GLD part of GLD/TLT was meant to capture this reluctance, which it has done. It seemed to me that if the market started to think Central Bankers were not totally useless, we would begin to see gold outperform equities. And starting in early 2025, that has been the case.

Plainly the much tighter energy market is causing the market to price in much tighter monetary policy.

If there is a problem with GLD/TLT it is the TLT side. US 30 years have been in a range for three years now. This should be surging higher in my view.

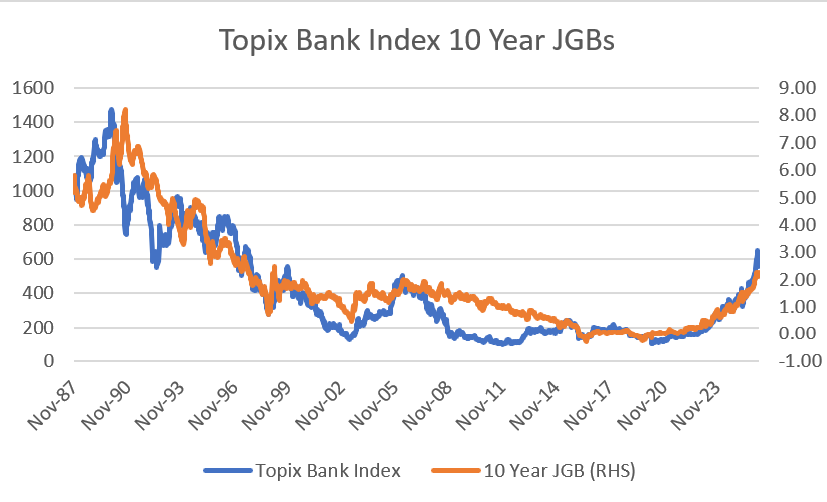

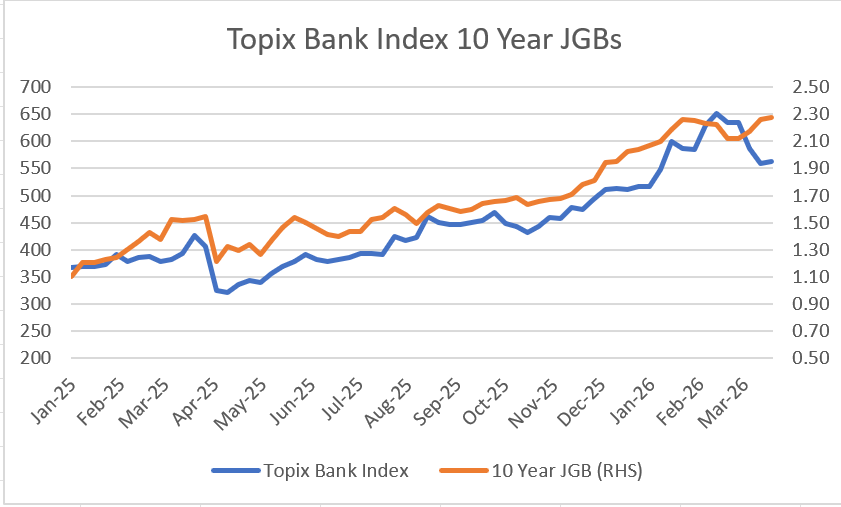

Also Japanese banks have diverged somewhat from 10yr JGB yields. Over the long term there is a very strong correlation.

But this month has seen a divergence.

You could make the argument that surging oil prices will lead to central banks tightening, and we then get a recession. This is what happened back in 2007 for example. In that case, you want to sell gold and equities and be long bonds. But talking a look at UK 10 year Gilts, and JGBs, the market is pretty clearly saying that politics will more likely lead to governments spending what they can. Clearly that is what happened during Covid and the energy shock of 2022, and what the voting public expect. It is also my expectation.

For me, the GLD/TLT trade still looks good, it just looks more likely the “negative” side of this trade needs to give more - that is weak equities and bonds. I suspect that is coming - just a bit of a sequencing issue.