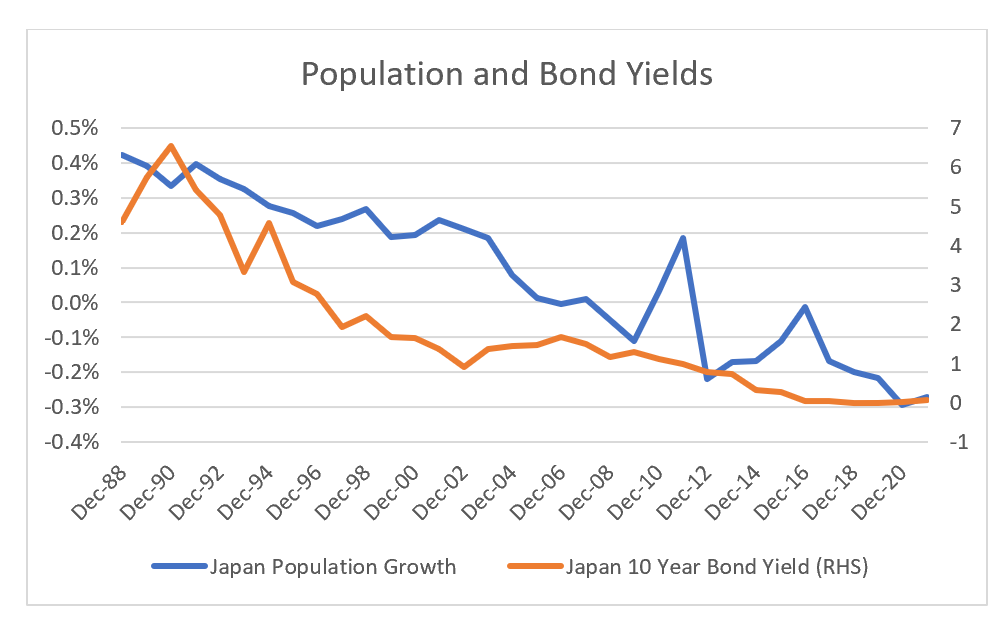

One of the favourite tropes of the deflationista crowd is that “demographics is destiny”. It argues that an aging and shrinking population is inherently deflationary, and that this has been the driver of the bull market in bonds. Exhibit A in this argument has been Japan.

The problem with this view, is that it is pretty easy to find data that proves the opposite. The UK suffered its lowest population growth in the 1970s and 1980s, even though inflation was at is highest. Population growth was lower than the great depression, but bond yields were much higher.

Politics seems to offer a much better explanation of inflation than demographics. The tricky thing about politics is that it means different things to different people, but if we place the dawn of universal democracy in the early 1900s, then we have only really had 120 years of “modern politics”. Prior to that period, almost everything could be described as geo-politics (or how do I expand my empire). In my understanding, in the aftermath of the Great Depression, the rise of nationalism, and then World War II, the electorate demanded changes to the system, to ensure full employment and rising wages. Almost any graph of income inequality over time will look something similar to below. If you invert this graph, you will get a chart that matches bond yields in the US and UK closely.

I understand the appeal of the demographics arguments for bond yields. Most fund managers and economists do not want to take a view on politics or invest on the basis of it, but the reality is that change is already happening, and it already affecting markets. Brexit offers a clear data set on this change. The referendum was essentially London versus the regions in England. Or Town versus Country. The Country (ie regions) that holds the whip hand. The Conservative Party has remade itself to this political reality, and recent council elections confirm this reality, where London councils turned to Labour, but outside of London, Conservatives did relatively well.

The swing voters that decide elections in the UK and the US now are in the rust belt/flyover regions of the world, and the politicians will appeal to these voters with policies that are socially conservative (anti immigrant, anti elite) and fiscally liberal (big spending, rising taxes on corporates) - or the opposite of what we have seen the last 40 years. So how much inflation can we expect? If austerity is politically impossible, then wages need to rise. How much? Well one way is to work out how much do wages need to rise to stabilise debt levels? Rising wages saw US Federal Debt to GDP fall from 120% of GDP to 30% of GDP. We are above 120% debt to GDP again now.

US Federal Minimum wage rose from USD 0.30 in 1940 to USD 3.25 in 1980. Today the US Federal Minimum wage today is USD 7.25, a similar increase implies a minimum wage of 72.50. A rapid rise in low end wages would also largely normalise high house to income ratios in the western world. The issue now is finding an asset or strategy that will protect wealth during a period of rapidly rising wages and inflation, and very likely government policies that might be described as “anti-business”. Good luck!

P.S. This analysis then leads to the question, why has Japanese government chosen to push deflation on its citizens for the past 30 years? I will attempt to provide a political analysis soon.