I was ordering my Pimms at Wimbledon, which I discovered would cost me £11 - and was extremely tempted to rant “You cannot be serious!”. But I sucked it up and paid. The next day I was drinking a £7 pint at my local, I looked at my phone and was assailed by financial commentators and substack writers with news that inflation was cured, and even deflation and rate cuts were looming on the horizon. Deflation you say? No one had told the drinking establishments I frequent. UK inflation index might be saying slowing inflation. But prices have not actually fallen.

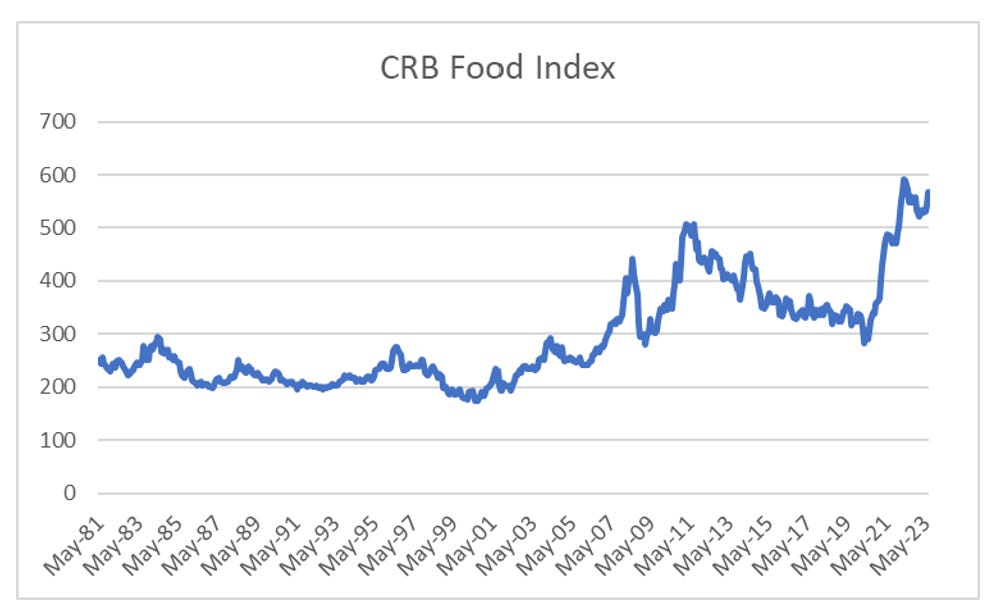

I suspect the deflation camp is looking at the period in 2013 to 2020, when food CPI stagnated after the steep rise from 2006 to 2012, and thinking that we are headed for a similar period of falling prices. UK food inflation has an upward bias, but periods of accelerated inflation occur when underlying commodity prices rise, and deflation when commodity prices are falling. We can look at the CRB Food Index to get an idea of trends there. I am struggling to see deflation.

For me there are three drivers to food inflation. One is low unemployment in the west. Given the fiscal impulse we see from both the UK and US government, I don’t see any reason for unemployment to rise. The US is also seeing Federal Government expenditure turn higher.

The second is that the ongoing Russian - Ukrainian war threatens the supply of huge amounts of grain. For wheat, Russia and Ukraine at largest and seventh largest exporters respectively. While there has been an agreement in place to allow Ukrainian exports to reach the market, it is subject to Russian whims. Ukraine is also a large supplier of coarse grain (corn) and vegetable oil (sunflower).

The final and most important reason was that China is turning into a net importer of food. China turned into a corn importer after the problems with African Swine Flu - but despite that being largely under control, and huge efforts by the Chinese government to reduce reliance on the US, China remains one of the largest markets for US Corn exports.

One other implication of China turning to a net importer of food is that it has also become an importer of rice. The world rice market has become increasingly reliant on India and Thailand as suppliers. Note, even though China is listed as exporting 2m tonnes of rice, it now imports 5m tonnes, making it a net importer.

India is the low cost producer of rice.

With India placing restrictions on rice exports, Thai rice prices have been rising again, and are back to levels seen during in 2021. During the spike in corn prices caused by the Russian invasion of Ukraine, many farmers used rice as feed as it was cheaper. Higher rice prices are likely to feed back into higher grain prices.

This could cause a negative feedback loop. China has been very successful in getting domestic pork prices back to pre-African Swine Flu levels, even if that still means Chinese pork prices are twice US prices.

Typically we look at pork to corn price ratios to determine the profitability of pork farming. In China we have seen farmers are record low profitability as corn prices have stayed high and pork prices low. I suspect this was due to rice being used as a substitute feed. This would also explain why China has become a net importer of rice in recent years.

India ban on rice exports is likely to cause food inflation to return to Chinese pork prices - which will likely put upward pressure on other grains. To me, it looks more like we are coming to the end of a lull in food inflation. Deflation while food prices are going up? You cannot be serious!