In a world of high and rising inflation and rising bond yields, Japan has been a oasis of calm. Its most recent CPI came in at less than 1% year on year, and its 10 year bond yield has remains around zero, as it has done for the last 6 years.

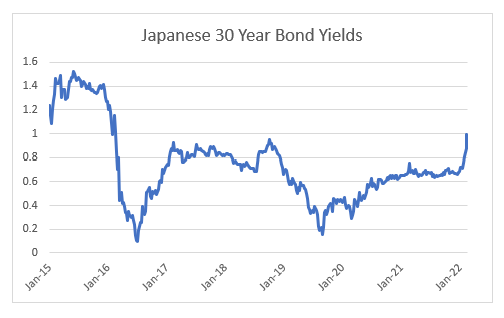

The BOJ is still by far the largest buyer of JGBs, but has tended to concentrate its buying up to the 20 years maturity. This has left the 30 year JGB to be more of a “market” reflection of inflation and interest rate expectations. In 2022, the 30 year JGB has sold off to yields last seen in 2016.

In my classic “free market” understanding of markets, the rising yields of Japanese 30 year bonds is a precursor to the BOJ reducing liquidity, and even attempting to raise interest rates. Using 3 month Tokyo Interbank rate as a proxy for BOJ monetary policy, we can see TIBOR rates rose in 1997, 2000 and 2006/7. Financial crises ensued after each time, name the Asian Financial Crisis, the Dot com bust and the GFC respectively.

So potentially rising 30 year JGBs are very bearish. However, I am also minded that JGBs have lagged some much more fundamental changes in the Japanese economy. Japan is no longer expensive. Japanese farmland that traded at 5 times the value of US farmland in early 1990s, now trades at a discount.

Furthermore, the stagnation in Japanese wages, and the rise in Chinese and other Asian wages have reduced the gap between Japanese GDP per capita and the rest of Asia substantially.

However, the biggest potential driver of inflation in Japan is whether the yen can continue to weaken against the Chinese Yuan. In 2021 and 2022, the Yen has managed to continue to weaken against the Yuan.

China recently recorded a record trade surplus, which suggests that Chinese yuan strength, and Yen weakness is yet to be a negative for China, suggesting that relative yen weakness can continue.

Putting it all together, market pricing is saying that either Japanese farmland is too cheap, the yen is too weak, or JGBs are the wrong price. The bigger question is whether reduced financial liquidity will cause the previous cycles of Yen spikes and financial crises to return, or is Japan now entering a prolonged inflationary upcycle?