Shorting long dated bonds has been a great trade. But the view, and the positioning that I am seeing is suggesting that most investors think that trade is done. If anything, I would say long bonds has become a conviction trade for many investors. TLT US is a liquid ETF that buys long dated treasuries. Typically, the net shares outstanding (shares outstanding less short interest) in this fund follows share price performance. Not in 2022. In 2022 investors have been buying TLT all the way down.

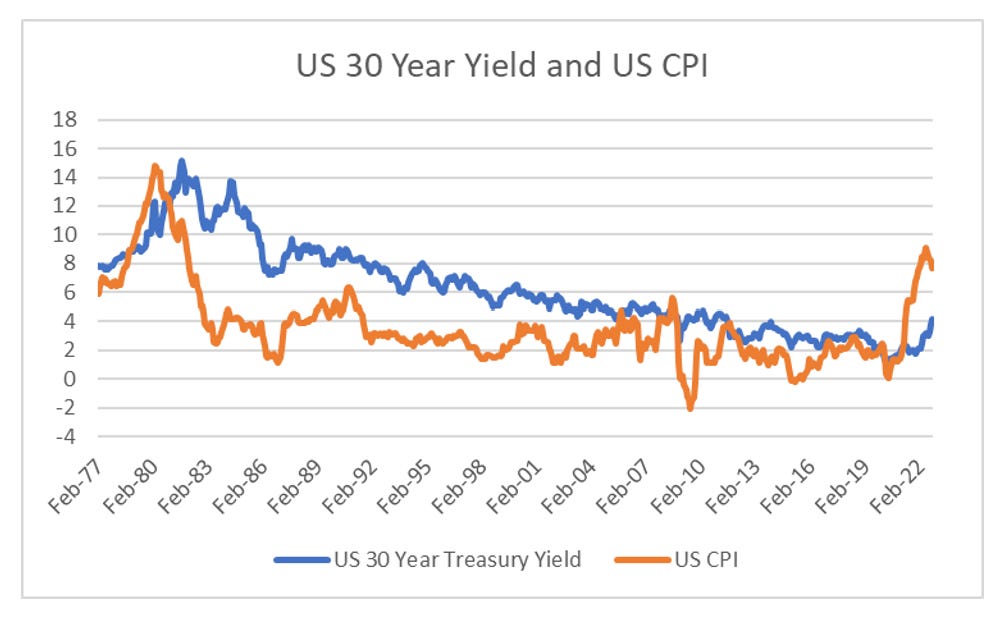

I find this enthusiasm hard to understand. US CPI is back at levels last seen in the 1970s, when the US 30-year treasury yielded north of 8%.

The reason that people are getting bullish bonds I believe is that the yield curve has inverted. And every time that has happened, you have a recession, and you want to get out of equities and into bonds.

Very oddly, Japanese long dated bond yields continue to trade poorly. For as long as I have been in markets, the JGB market has acted as a very good lead on US bond markets. Not only has it been prescient in leading the US bond yields lower from 1999 onwards, in 2020 the JGB market was also prescient in signalling the future US treasury sell off.

What does the JGB market see that the US doesn’t? When I think about the Federal Reserve politically, the one type of inflation that they have to react to is food inflation. Food inflation is a very regressive tax, and is the one type of inflation that has proven track record of getting people on the streets.

Since 1980, food commodity prices have generally moved with raw industrial commodities. That is, if you could create and industrial recession (i.e. raise interest rates), that would be enough to get food prices to fall. And as most farmers will tell you, fuel costs are the biggest cost for most farm (fertiliser tends to follow natural gas prices).

And here is the problem. China is now the world’s biggest importer of food, and it has much higher prices than the US. Pork, which is the most consumed meat in China, is now 3 times more expensive than the US market, and has recently doubled in price. As Japan is also a large importer of pork, perhaps this was the reason the JGB market sold off before the US.

While pork and African Swine Fever (ASF) gets all the attention, China has also very quietly become a large importer of beef. Monthly data from the US shows how imports rose during ASF but have never really fallen off. These numbers understate Chinese demand for beef. On a global basis, China imports more beef than the rest of the world on a net basis (US and EU are both large importers and exporters).

Again, China beef prices are at a premium to US prices.

In essence, I am saying that China is exporting food inflation to the rest of the world, and I don’t see that ending at the moment. JGBs seem to agree - and when I look at the index value of US Food CPI on a log basis, I keep thinking that is says interest rates are going higher not lower. I have used log basis so you can see the inflection in food prices is close to what was seen in the early 1970s.

In essence, I am saying that food inflation has moved from being cyclical, driven by energy prices, to secular driven by an urbanising China. Secular food inflation implies POLITICAL pressure to have higher interest rates. US treasuries look a short to me, just as everyone has gotten long.