TEXAS TEA PARTY

Shale discipline looks here to stay

One of the attractive features of shale is that it can rapidly adjust to changing prices. After the first oil price crash of the shale era in 2014/5, US shale producers cut production for a year or so, but as oil prices recovered US production rose again. US oil production was at all time high just prior to Covid-19, but rapidly fell. Production is beginning to edge higher again.

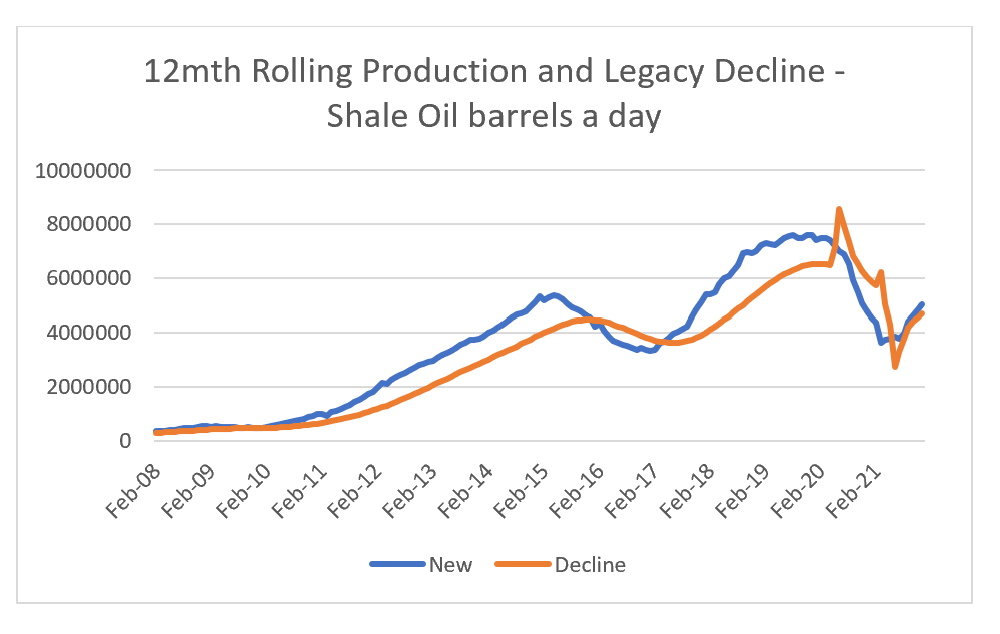

Shale oil production growth relies on two separate factors. The first is how much new oil is being drilled, and the second how much oil production started a year ago is rolling off. 50% of all the oil from a well comes in the first year, leading to high decline rates. Production growth occurs when new drilling is higher than legacy decline, but the more production growth, the more future legacy decline. What we have seen with shale oil is that production falls very quickly when new drilling declines for about a year until legacy declines fall to a lower level, and production can begin to grow again. New production is beginning to outpace legacy decline again.

When we look at other indicators, we can also see drilling activity has been increasing in the US again. The number of rigs being deployed has been steadily rising over the last year.

The conclusion would seem to be that higher shale production is likely, and with it the same downward pressures on the oil market that has been apparent since 2014. However, one feature of the shale market has changed radically. Shale producers have been rapidly running down their stock of drilled uncompleted (DUC) wells. I think of DUC wells as a form of inventory, wells that are stored for future use.

The Permian has been the dominant region over the past five years. Out of the oil collapse in 2014/5 we saw that oil companies drilled far more wells then they completed (sometimes it was part of their lease requirement to drill a well within a certain period, or just to show growth to investors). This behaviour has changed, as drilling now lags completion.

One feature of shale oil drilling is that it tends to also produce excess natural gas. During the boom in Permian drilling, negative pricing in natural gas started in 2019 as producers would pay for someone to take away the natural gas. The break higher in natural gas prices in 2021 confirms the changed nature of shale drilling.

For many years, excess supply of natural gas and oil from the shale region made the energy sector investing very difficult. Supply now looks to be under control, so investors now need to mainly consider demand. Governments are regulating against fossil fuels, which makes forecasting demand trickier than it was. But falling demand is no impediment to rising returns, as the long term performance of tobacco stocks has shown. The Texas Tea Party may be one of capital returns rather than growth, but that is still a party.