With the failure of Silicon Valley Bank (SVB), there is a widespread view that the Federal Reserve is done with its rate hiking cycle. Certainly, the bond yields of long dated Treasuries and JGBs have fallen in recent weeks.

This may be true, but I think this more muscle memory from the GFC, than a true reflection of the likely inflation and interest rate market outlook. For new subscribers, there are many detailed explanations in older posts, but in essence I am arguing that in 2016, we saw a political change, that began to favour workers over corporates. That is it became political unacceptable to put all the burden of economic adjustment on workers and wages. In fact policy is now geared to raising “real wages”, which means tighter monetary policy, and policy geared to ending speculation. The destruction of Chinese property developers was one feature of this, and I would say the demise of SVB is another. The end game for me is something like the 1970s, with strong commodity prices and higher interest rates as wage inflation gets out of control. We are still early in that trade, if correct.

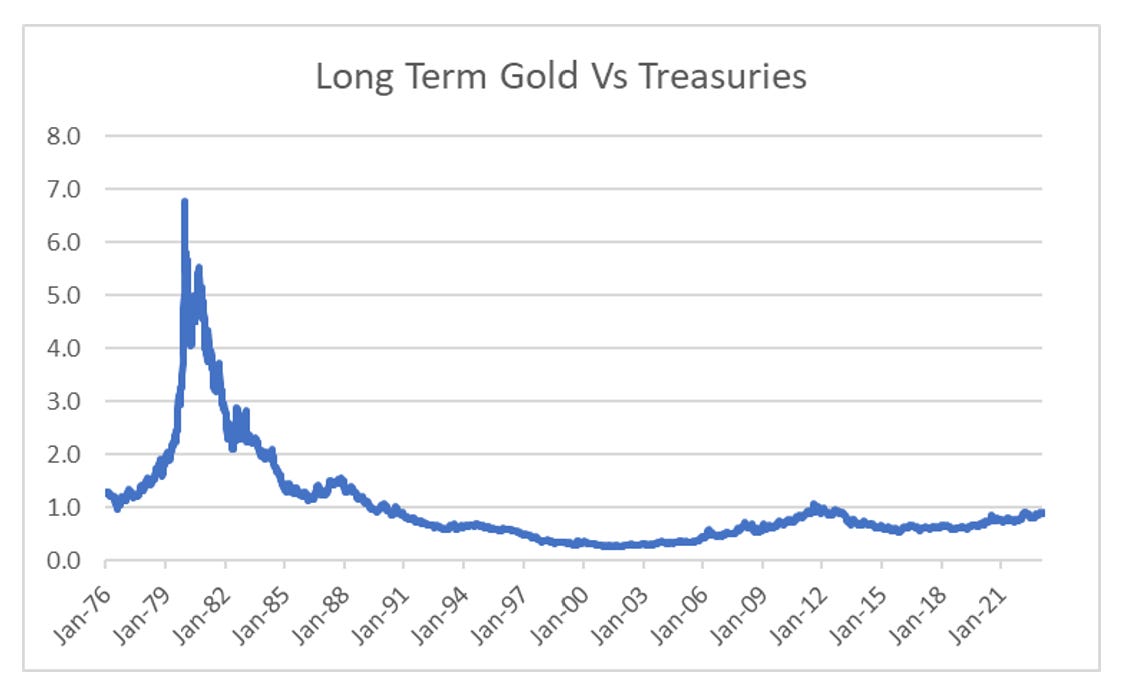

The recommended trade for this view is long GLD/Short TLT. On Friday as TLT rallied 3 percent, GLD also rallied 2%. The GLD/TLT pair did no inflect deflationary in anyway.

If you are tin-hat, armchair twitter, look at me style substack writer, you may well wonder how GLD/TLT faired in 2007/8 period. Well I show it below. Actually, gold did well until late 2008, and then you wanted to be long bonds, and then back into gold.

So you might be looking at this and thinking this is random. But actually, the market is not random in this case. What I would argue is the market is sending a very clear signal, its just that you are not ready to receive it. What is the market saying? It is saying that China, not the Fed, is the market and government that sets global inflation trends. But not via construction, or auto and luxury sales, but via food (please see my food inflation posts for more detail). As mentioned in 2016, China move pro labour, and has been more successful at raising wages than other nations in recent years. China now has higher food prices in the US, and is large importer of food. So unless China devalues, food inflation will remain an issue globally.

Why is this an issue? Well politicians are very simple creatures. They just want to get re-elected. If people are worried about food inflation, then pressure will be on central banks to get food inflation down, with the easiest way to do this is via tight monetary policy and strong currencies. So over the last year, food inflation has been strong.

And to counter this, the Fed has pursued a strong dollar, tight monetary policy regime.

The problem is that it has not caused China to devalue. And with China exiting Covid restrictions, and the war in Ukraine continuing, the failure of SVB is going to have no effect on food inflation. In anything, US dollar weakness will make things worse.