I am surprisingly often asked if I am going to launch a new hedge fund (to be honest, mainly by my old brokers who have a strong financial interest to see me get back in the game!). As the barrier to entry for most people to starting a hedge fund is capital and brand name, neither of which is a problem for me, most people cannot understand why I have not done so already. I have decided to put my thoughts to paper, so at least people (or my old brokers at least) can understand what issues I am thinking about. First of all, I think people need to understand how the hedge fund industry has changed in the time I have been involved with it.

Prior to 2000, hedge funds tended to be extremely niche investments, and typically pretty small - USD200m would be a big fund. Then around 2001/2 the hedge fund industry exploded in size. The first reason was that after the dot com bust and then the GFC, the 3 year rolling returns of being invested in the S&P 500 went negative during the 2000s.

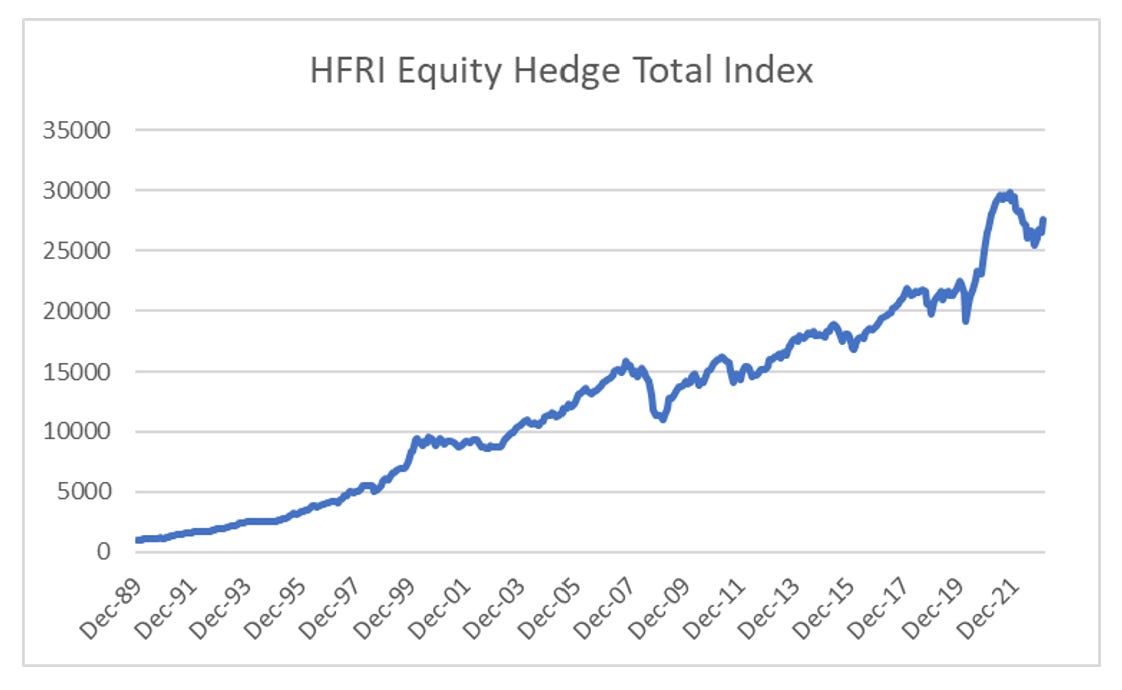

During this period from 2000 to 2002, hedge funds did not drawdown, which made their relative performance really stand out.

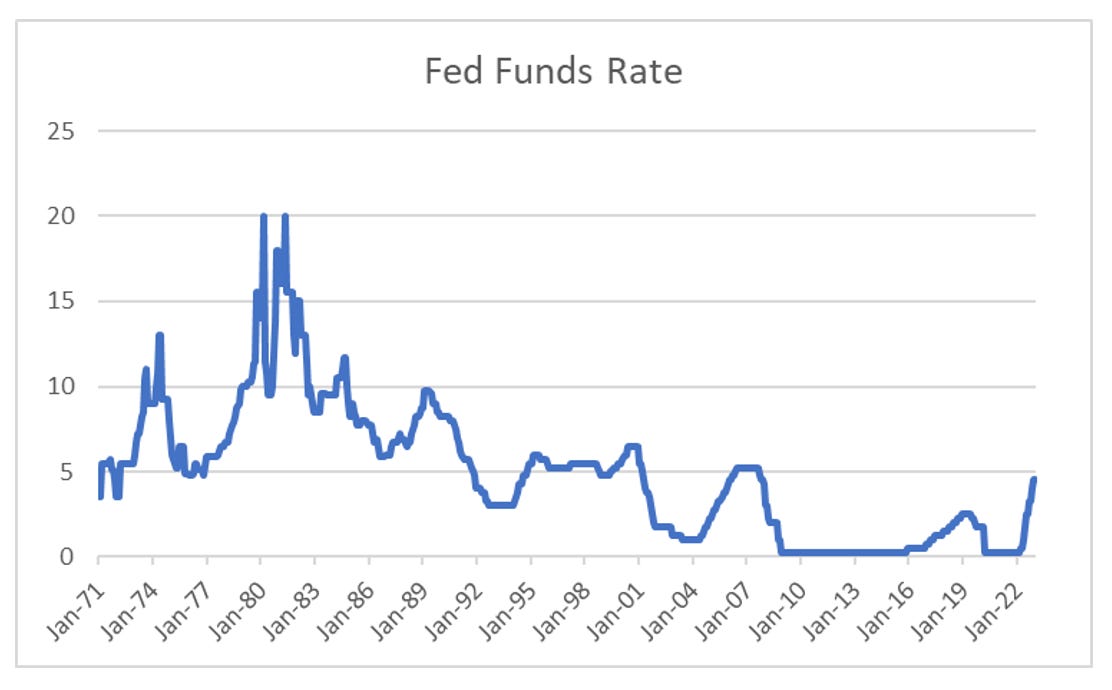

The 1970s also saw poor returns to being invested in the S&P 500, but at least at that time investors could put money in high yielding money market funds. In 2001, the Federal Reserve put interest rates at very low levels and for the next 2 decades, you rarely got paid anything for holding cash. . Meaning that holding cash also looked very unappealing. This combination of low interest rates and poor equity returns were fantastic tailwind for hedge funds.

I joined GAM in London in 2002 as the hedge fund boom was really starting to take off. One observation I would make is that 2002 boom in hedge funds, was really a boom in fund of fund businesses. These were businesses that invested into hedge funds on your behalf. At the time, they were selling their superior knowledge of hedge fund strategies, as well as the relationships with the best hedge funds, who were often closed to new capital. GAM itself had a fund of fund business that was also doing well, which as far as I know was the reason that UBS had purchased it. The boom in “fund of fund” business led to a boom in hedge fund start ups. The fund of funds had so much capital flowing in, they needed new hedge funds to invest in. During the early 2000s, almost any manager with a decent long only fund would also launch a hedge fund as a side business. Bloomberg shows how launches peaked in late 2000s. This was the glory days of hedge fund industry.

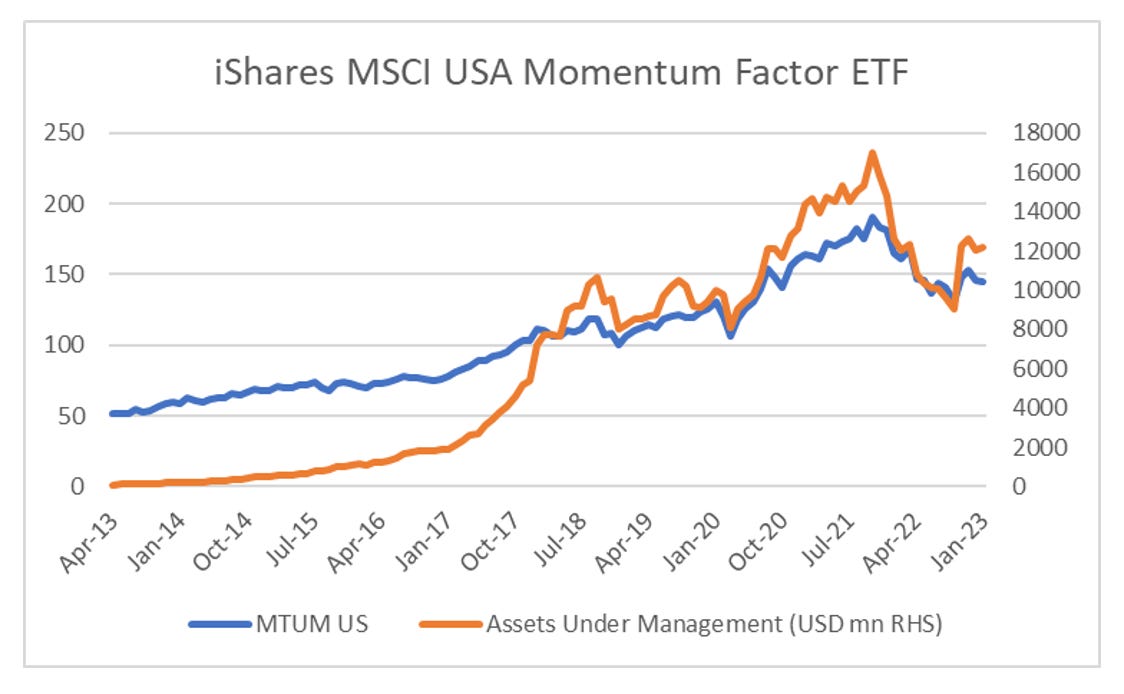

Why have launches fallen so much? Well if you look back at the HFRI returns above, you can see that hedge funds did poorly in 2008. That is they did not actually hedge the market at all. It was around this time allocators began to say things like “hedge funds are a fee structure looking for an investing strategy” or “it is not called equity short/long for a reason” - the implication is that hedge funds are always long biased. The other big reason for falling hedge fund launches was the decimation of the fund of fund business. Many fund of fund were invested in Madoff, which essentially shredded their reputations for due diligence and destroyed the seed capital for new launches. Ultimately this led to institutional investors cutting out the fund of funds, and going directly to hedge funds. This changed the industry dramatically. Prior to 2008, if you were the best performing hedge fund, you would expect to see capital inflows, regardless of how you generated that return. Post 2008, in my view, allocators would be looking at how that return was generated, and whether it could be replicated with low cost strategies. This led to the rise of the factor investing and ETFs. One of the most common strategies that hedge funds have used to generate returns is momentum. The iShares Momentum ETF would replicate this strategy for 0.15% expense ratio, with daily liquidity and 100% transparency. This makes the value proposition of a hedge fund with monthly liquidity, 2% management fee and 20% performance fee and limited transparency difficult to justify.

The other problem that the death of the fund of fund business caused was that institutional investors became aware of the commonality of positions across hedge funds. A hedge fund portfolio may have investments in many different hedge funds, but if all those funds had 10% positions in 5 different FANG stocks, there was no real benefit, and large costs/fees to investing in hedge funds. This created a huge problems for hedge funds, as FANG stocks massively outperformed the S&P 500 from 2014 to 2021. If hedge funds used the FANG stocks to achieve good returns, it made it easy for allocators to pull money, and if they did not use FANG stocks, they needed to generate returns from underperforming stocks. That is industry and fee pressure was making it very hard to outperform.

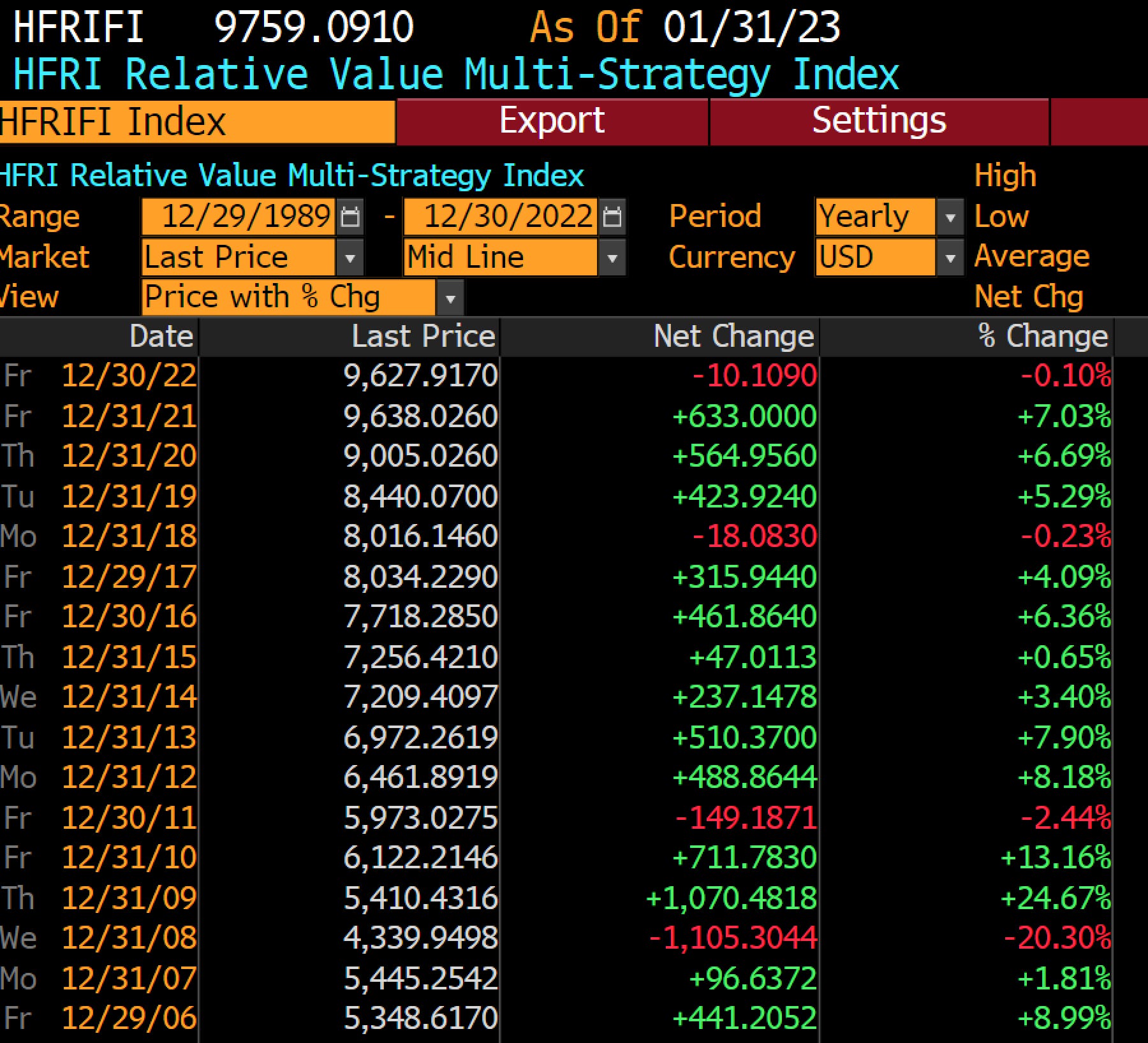

Post 2008, there in one thing that has really kept the hedge fund industry afloat And that has been low interest rates. Many allocators would put money to work in strategies that could generate “bond +” returns with little volatility. This led to huge growth in “pod investing”. This is a from of fund of fund investing, except it is all brought inside one firm, and a lead portfolio manager will have total transparency on positions and capital allocations. They tend to run under a “rank and yank” system, where underperforming fund managers quickly lose capital or even their job. Using the HFRI Relative Value Multi-Strategy Index as a proxy for returns, you can see you typically make bond like returns, but with the risk of large drawdowns. If interest rates keep rising, I don’t see how these strategies can attract capital.

The story of hedge funds (and I am mainly talking about equity long/short funds) has been a boom era in the 2000s, followed by a long shakeout and professionalisation in the 2010s. The professionalisation of the industry has meant that hedge funds with superior systems have been able to raise larger amount of capital. During the 2010s, I developed a currency based investment system which was oddly enough based on looking at how other funds had failed, and attacking that weakness. This strategy worked well until 2016, and not so well since. When I look at the funds that have succeeded over the last ten years, I find that many of the systems use regulatory arbitrage to generate an edge. This creates two problems for me. One is that is extremely hard to replicate. And secondly, these models are always at risk of legal and regulatory change, which is very hard to judge. These models will be the subject of a future post. And to answer, the question in the title, you should only launch a fund if you have an edge in my view.