RETHINKING THE STAGFLATION OF THE 1970s

And why interest rates are so low now

The common view of 1970s was that bond yields in the US were so high due to inflation being so high. With that logic, the very quiescent inflation from 1990 onwards explains ever falling bond yields. However the recent spike in inflation, coupled with very large US government deficits would seemingly imply much higher treasury yields. That has not happened.

It is however possible to analyse the experience of the 1970s in a different way that explains why bond yields have fallen, and continue to remain low. Prior to 1970s, the world had been on a gold standard, in one form or another. Using data from the World Gold Council, we can see that US and the Rest of World both saw rising gold reserves until 1940. World War II then impoverished most of Western Europe. As Europe recovered post World War II, gold began to leave the US and return to Europe.

Falling gold reserves was typically taken as a negative signal, as international investors in particular would question the ability of a government to maintain the pegged (to gold) exchange rate. Hence, perhaps the stagflation of the 1970s reflected particular weakness in the US, more than a global phenomenon? If that is the case, then we should see much lower bond yields in countries with rising gold reserves in 1970s, countries such as Japan, Germany, Switzerland, Italy and the Netherlands. There is some evidence of this, with the most striking divergence being in Swiss bond yields and US bond yields during the late 1970s and 1980s. Swiss bond yields rarely rose above 6 percent, compared to a peak of 15 percent for the US. Switzerland and US had suffered little industrial damage during World War II, so were closer economically than most of Europe and Japan.

This difference in bond yields is largely explained by the surging value of the Swiss Franc in 1970s.

The surging value of the Swiss Franc led to much slower growth and recession in 1970s. Similar problems were seen in other export dependent economies.

The gold standard had worked exactly as it meant to with countries building up gold reserves having lower inflation and more stable currencies, while the US saw gold reserves fall, and suffered from more inflation and a weaker currency. The problem that became apparent to everyone in the 1970s was that the US was “too big to fail” - both economically and militarily. Kissinger convinced the Saudis to recycle their trade surpluses into treasuries, and so the idea of a “petrodollar” began. Saudi foreign reserves began to climb, overtaking Japan in the mid 1970s.

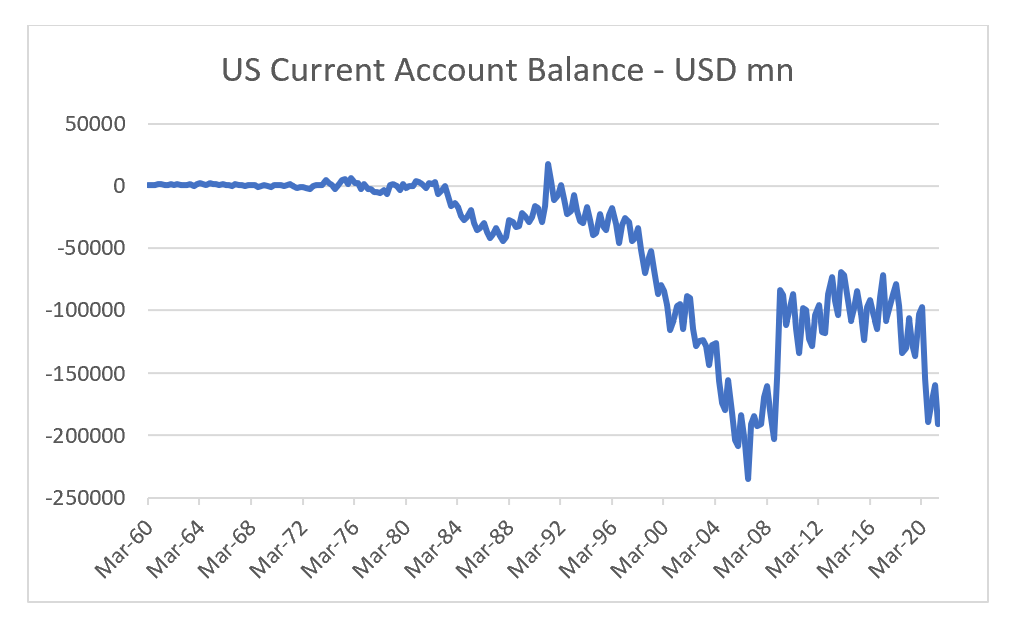

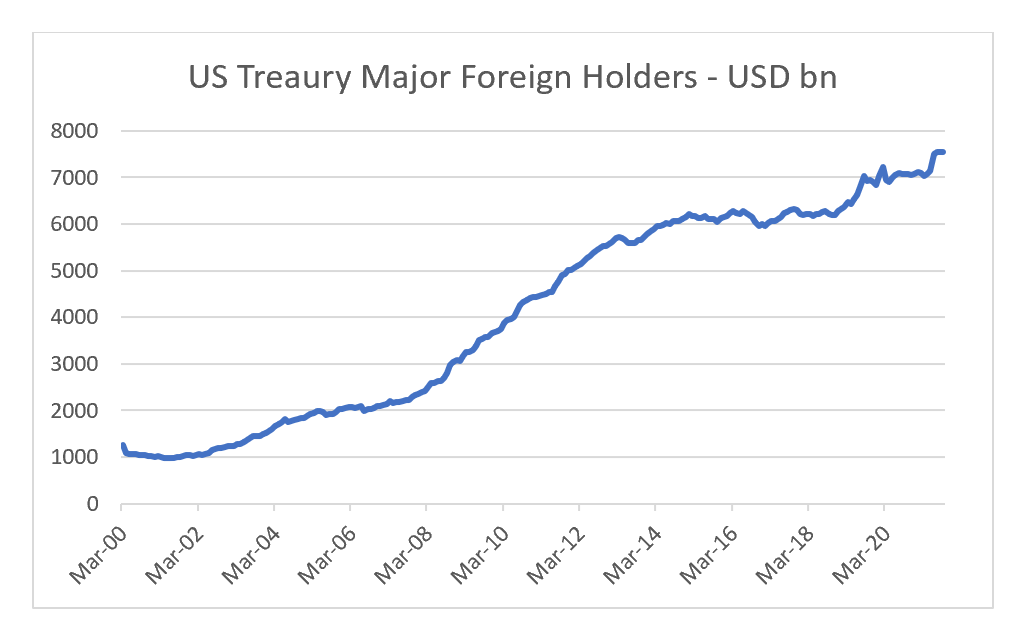

Moving from gold to US treasuries as the main foreign reserve holding had big benefits. Firstly, it was now impossible for the US to default, as it could print whatever it needed. This has allowed the US to expand its current account deficit.

This excess consumption is then recycled back into US treasuries, mainly through the growth of foreign reserves. That is governments of exporting nations choose to support the dollar and US growth, rather than allow their currencies appreciate.

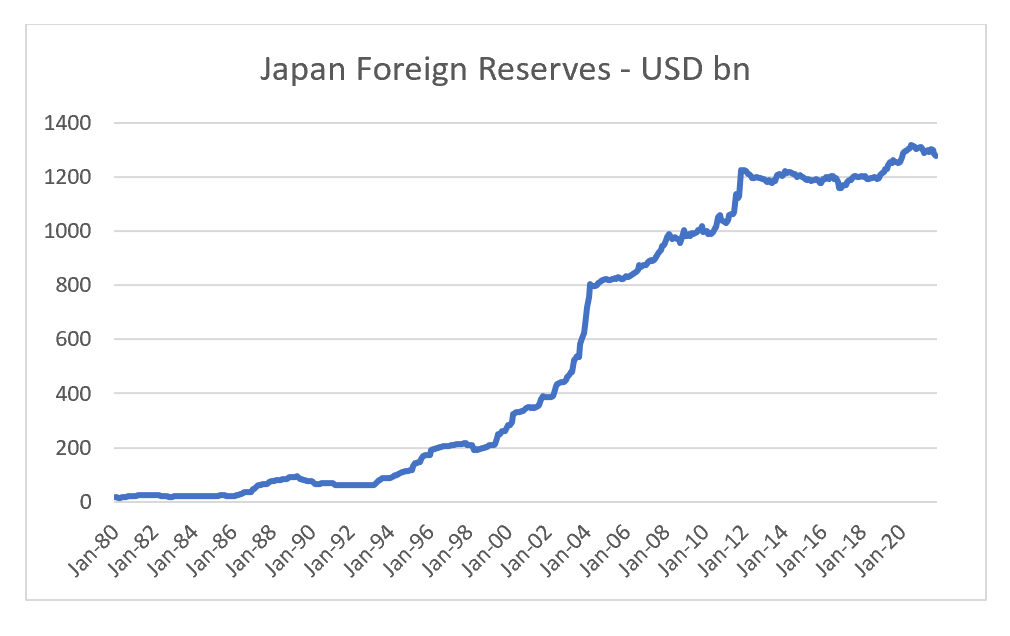

For the US, moving from the gold standard to a fiat currency system removed the possibility of defaulting on its liabilities. The only risk, was currency weakness. But with the US being the consumer of last resort, and in many ways too big to fail, exporters are left with little option but supporting the US dollar. Japan in particular has pursued a continual Yen weakness policy since the mid 1990s. This policy has led Japan to have a very large build up in foreign reserves, mainly held as US treasuries.

The inflation mandates of the central banks of exporting nations imply they need to keep their currencies weak. Keeping their currencies weak, implies supporting the US dollar, and treasury market. This seems mutually reinforcing to me.

How could this cycle end? A move back to a gold standard seems inconceivable to me. But there are signs of some movement away from buying US treasuries. If this is the case, then we are the beginning of a huge change in financial markets. This will the subject of my next post.