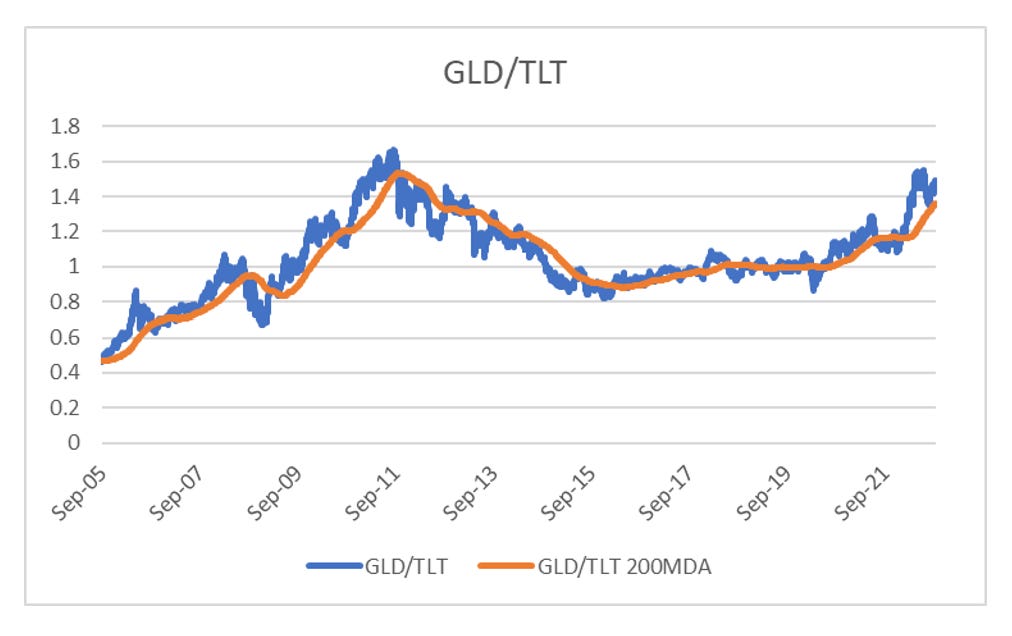

I think politics is turning pro-labour over pro-capital. Biden and the Democrats seem to be doing surprisingly well politically and wherever I look at the world politics, the response to rising nationalism has been more pro-labour policies. My argument is that focusing on raising real wages will lead to strong currency policies (already seen in most of the world, except for Japan - but maybe Japan is not a real democracy), and rising interest rates. The day to day market test of this of this theory should be the gold ETF outperforming the treasury ETF (GLD/TLT). What I really like about this ratio is that is picked up the deflationary inflection back in 2011, well before the market, and it picked up the inflationary trend during Covid shock very early. The trend still seems up to me.

Politically, I think it still makes sense to bet on more inflation, and for bonds to be weak, that is to be buying GLD US and selling TLT US, and market action confirms this. What has been extraordinary has been the shares outstanding in TLT and GLD show investors doing the exact opposite. Shares outstanding in GLD are almost back to pre COVID levels, while shares outstanding in TLT have more than doubled this year.

In general, I usually take great comfort in seeing investors taking the other side of a trade. Normally this is a very good sign, but grey hairs and bitter experience has taught me I should always take a good look at what investors are looking at to to take the other side of trade. Probably the most obvious place to look is the oil market. WTI has fallen in a straight line from 120 to 86 USD a barrel in the last few weeks.

The problem is that other energy markets, and particularly natural gas show little of the weakness seen in oil. When we look at US oil more closely we find that looseness in US oil market has been driven by a big release from the Strategic Petroleum Reserve (SPR). My guess this continues until the mid-terms held on 8 November. US oil inventory is at 20 year lows, something I associate with a tightening market, not a loosening market.

From a macro perspective, a strong dollar has normally meant deflationary trades work better, and would argue to being long TLT and short GLD, which may be driving the investors positioning shown above.

However classic cross rate indicators such as GBP/JPY, which have a better track record of catching deflationary turns still indicate an upcycle in place. GBP/JPY has been much more sensitive to deflationary trends than DXY, picking up the Japanese recession in early 1990s, Asian Financial Crisis, GFC and China devaluation fears in 2015.

So why are markets so keen on deflationary assets? For the last 40 years, the inflationary 1970s made politicians and institutions choose recession over inflation. I think we are now in a world where politicians choose inflation over recession, and politicians that make that choice are benefiting politically. Bonds still look like a short, commodities a buy to me.