I love patience, I hate stagnation. I have been talking about a pro-labour (anti-capital) move in politics and markets for some time. For nearly 18 months, I have been recommend long GLD, Short TLT. The short TLT part has been much better than expected, but GLD has held up much better than I would have expected given the level of monetary tightening, but that was the point of the GLD/TLT trade. The fund manager in me knows that when you have a winning the trade, the key is patience. The problem is publishing versions of the same idea on substack is a bit stagnant in my view.

The GLD/TLT trade has a long way to play out. Ultimately, I think this plays out in a 1970s style spike in yields, and rising commodity prices. We can proxy this using a US treasury return index and gold prices. As I have pointed out, TLT is a great product to short in rising rates environment, as it has no pull to par. The implication, is that we are still in the foothills of this trade. Soaring inflation, or potential default could get us to the end game here (or some combination of both).

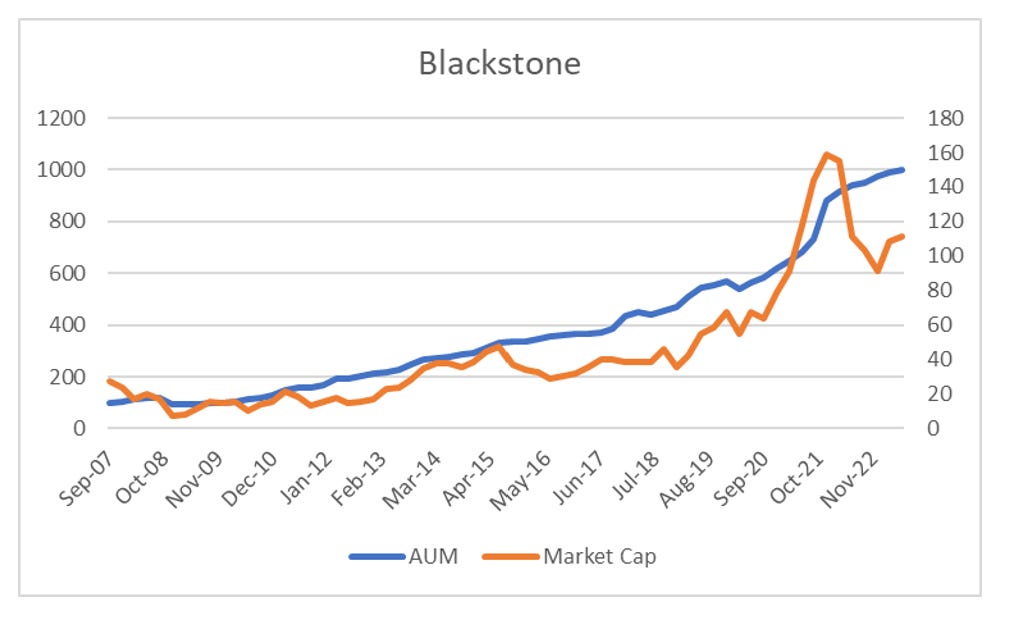

Even though Long GLD/short TLT is a great trade, it is NOT the basis of a successful fund. If your basic fund structure is GLD/TLT, a semi-competent allocator will just go out and replicate it directly (and avoid paying fees to me). This is the brutal reality of the fund management industry - and cannot be avoided. So how do you take an idea of GLD/TLT and turn it into a marketable product? The first thing you need to do is put yourself in the shoes of the allocator. What do the ideas behind GLD/TLT mean for the allocator. Well as mentioned in my last post, AUM is still flowing to Private Equity. Blackstone has USD 1 trillion of assets, and total industry estimates of USD 12 trillion.

Private Equity offers many benefits. It uses debt to juice returns. It also uses internal valuations, so at least gives the appearance of stable returns, and as pointed out again in the last post, with long term bonds only yielding slightly more than inflation, the temptation to put money to work with private equity is strong.

The problem of course is that GLD/TLT in its extreme form implies that private equity is, to use a technical term, fucked. The extreme form of GLD/TLT implies not only rising interest rates, but rising taxes, and rising costs. More of the profit pie will go to labour, and costs should rise across the board. This is already affecting other industries that have been reliant on financing to grow, such as REITS.

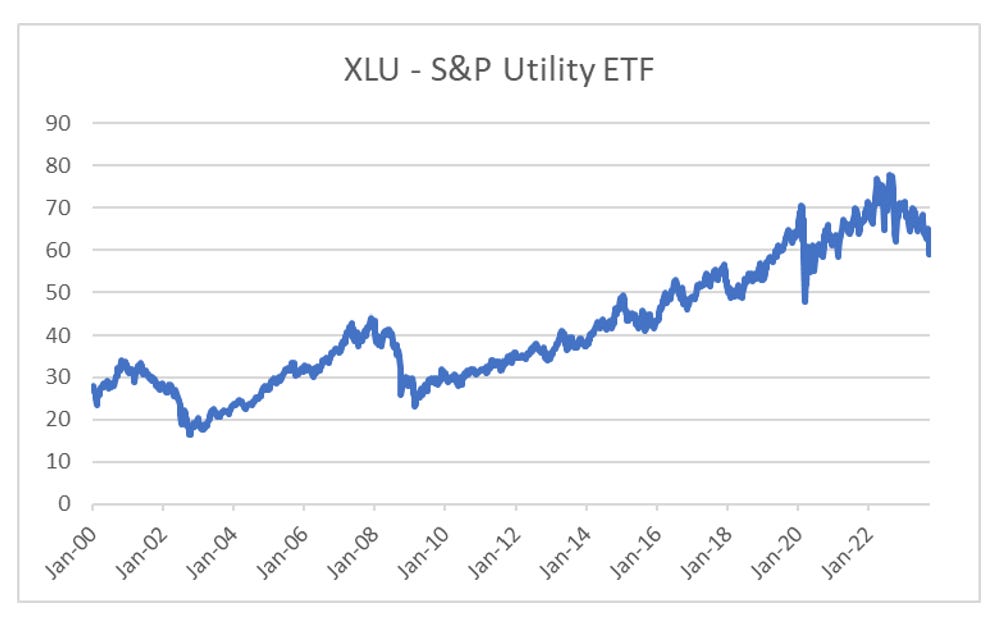

Or even boring, easy to leverage businesses like utilities.

So suddenly, I can see an investment strategy that has an attractive business strategy. Building out short bias fund that makes money when private equity lose money. Why is this a good business strategy? And semi-competent allocator should be worried about their allocation to private equity. What if interest rates go to 10%? The problem is that private equity money is locked in, and difficult to exit. An allocation to a fund that makes money when private equity goes wrongs makes a lot of sense. All of this might sound theoretical, but I am speaking form experience. When I started out in fund management, I started in emerging markets in 2002, as I knew China was the next big thing. As it worked out, this was perfect timing, and I benefited from the huge bull market from 2002 to 2007. But by 2010, I knew China was, to use a technical term, fucked. So basically went out and shorted China related names, with a view that a China crisis and devaluation was inevitable.

I had a far better business being bearish on China from 2011 onwards, than ever had being bullish. Why? Because allocators had big positions in emerging markets and commodities that they could not easily sell. My view was that China would follow Japan and Korea and devalue it way out of credit problems. Instead China has chosen to close the capital account in 2016, and the short emerging market trade became extremely volatile.

After taking a few years off, to think about why China chose not to devalue and what that means, I have a new pro-labour/anti-capital model that I use (anti-capital politics chooses not to devalue as it reduces real wages), which means that currency devaluation is not the destructive force in markets anymore, but rising interests rates are. The continuing sell off in JGBs confirms this view to me.

So what next? Well I am now going to build an “anti-private equity” portfolio - just as I built an “anti-China” portfolio back in the day, which will combine the use of equities, bonds and (maybe) currencies. Once I have built that, I will provide a monthly newsletter talking about positions etc. This will only be for paying subscribers. And if I like the look of the portfolio, and there is a market appetite for it, then I may launch a fund. In simple terms, this substack is moving from theoretical to practical. Exciting times!