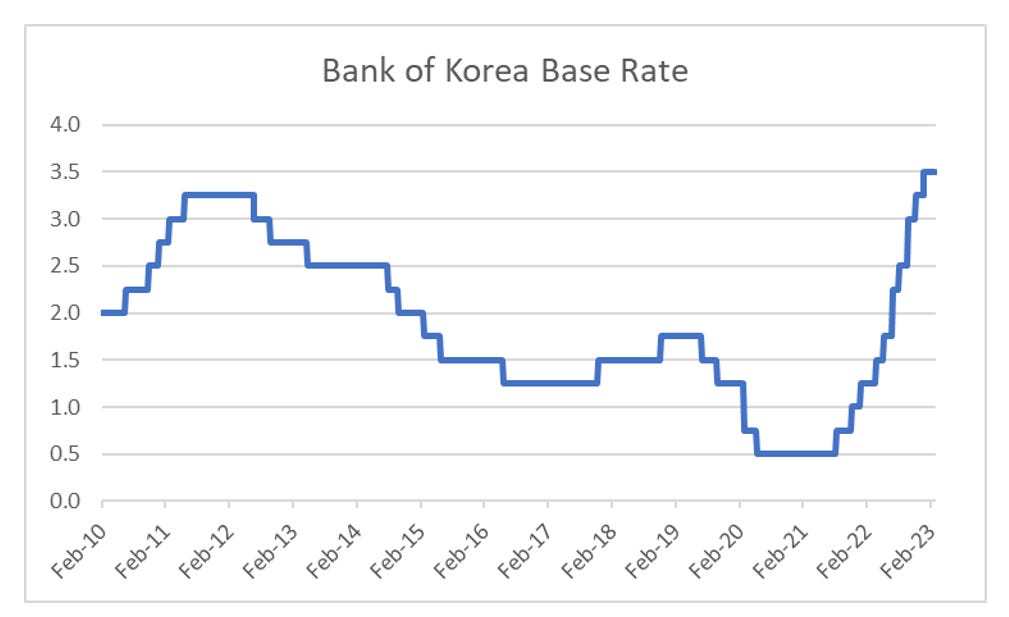

I have written extensively about autocallables, so feel free to click on the tab on my home page. Historically, the main risk of autocallables is that they break through lower barriers, and leave the owners of autocallables out of pocket, and cause equity volatility to spike as structural sellers disappear. The biggest single market for autocallables is South Korea. They really took off when interests fell in 2010 onwards.

Historically issuance of autocallables has fallen after market weakness (market falls destroy capital, which takes awhile to rebuild). 2015 saw a sharp decline in issuance after problem with the HSCEI market that fell 40%, and then again after Covid. Recently issuance has slowed, rather than a sharp decline. I suspect one reason is that with BOK raising interest rats to 3.5%, the 5% typical yield on an autocallable in Korea is losing its lustre.

However reduced issuance does not mean that the amount of autocallables outstanding has fallen. In a typical down to sideways markets they just sit there waiting for markets to either break up or breakdown. If that does not happen then they will naturally expire in about 3 years time. However, the recent issues with Credit Suisse may change that.