Recently there has been some sizable falls in commodity prices. Combined with the flattening yield curve, the drumbeats of recession and deflation have been rising across the financial commentator jungle. Key long term measures of long term inflation have seemingly inflected lower. Spikes in food prices such at in 1996, 2007 and 2011 have led to very deflationary market outcomes; the Asian Financial Crisis, the GFC and the Euro-Crisis respectively.

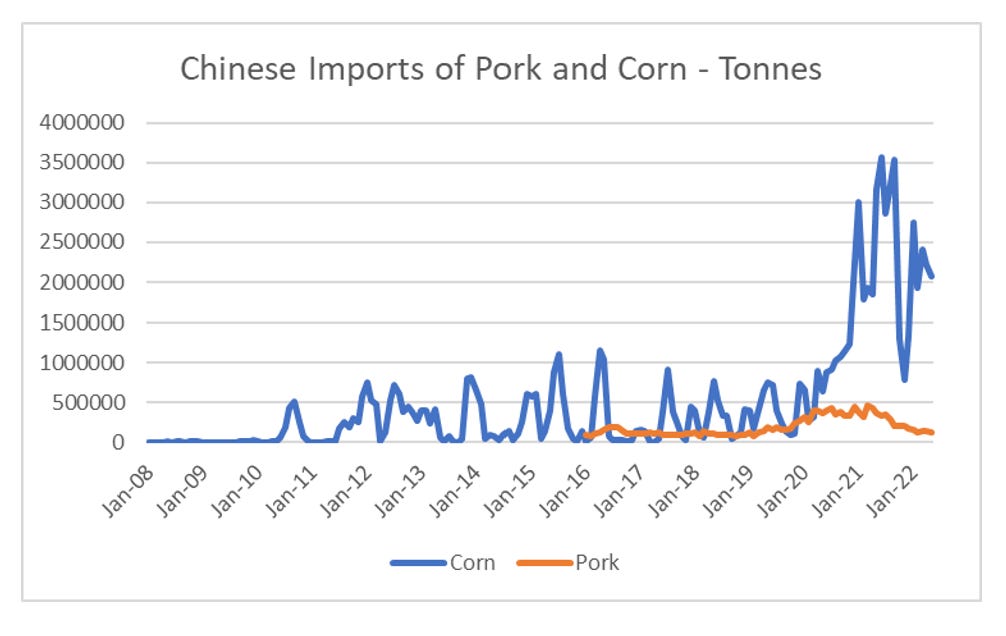

From a purely technical analysis perspective I can understand the urge to be bearish commodities from here. The problem is that underlying data on key commodities have actually begun to inflect bullishly. Within the food space, corn is probably the most important crop, from both a volume perspective, as well as a feed for livestock. The initial stage of the spike in food prices was driven by China becoming a large importer of corn and pork.

When we look at corn prices, we see that US prices have been much weaker than Chinese prices over the last month. If you were bearishly minded, you would note that US prices led Chinese prices in the last down cycle in 2011 to 2017

The problem with the bearish narrative is that Chinese pork prices have suddenly begun to spike again. This was the catalyst for the first rally in food prices. With the big increase in Chinese imports of both pork and corn, its seems to me that its hard to push the food deflation button when Chinese pork prices have doubled in last 3 months, and are at the highest level outside of the African Swine Flu crisis.

Energy markets are correctly seen as having an outsized effect on inflation and inflation expectations.