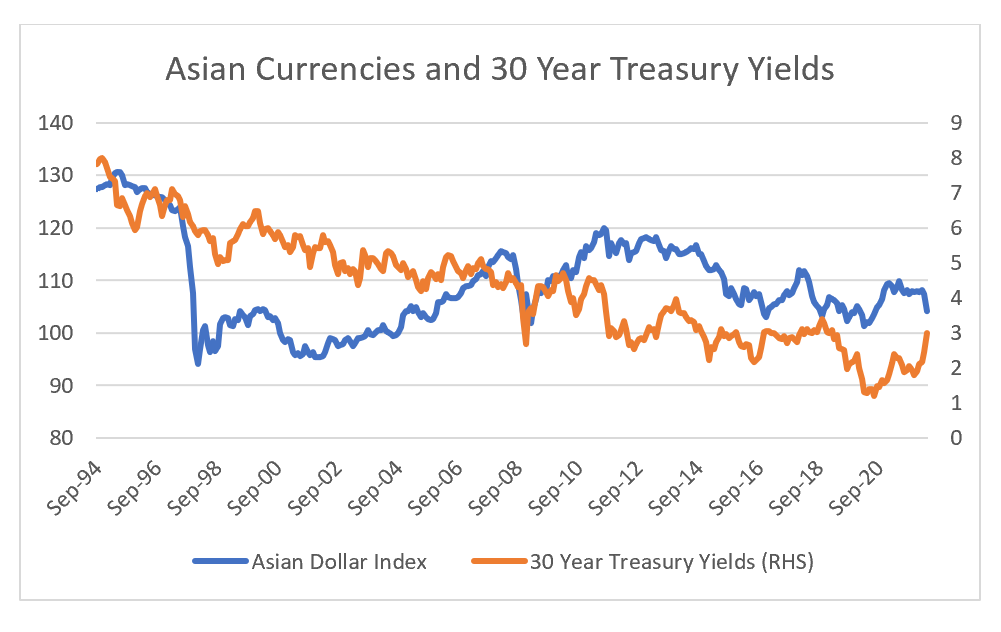

One of my old macro rules was to never be short treasuries when Asian currencies were weakening. Other ways of saying this is a strengthening dollar is a sign of weakening growth, or liquidity issues, all of which are deflationary. Bonds have tended to do well the US dollar has had significant strength during the Asian Financial Crisis and the GFC. Asian currencies have been conspicuously weak this year.

Asia these days is dominated by the Chinese economy. 1 Year Shibor Rates have been moving lower for over a year now, and recently the Chinese Yuan has begun to weaken, both classic deflationary signs.

If you throw in Covid and the long forgotten issues with Evergrande and other property developers, then you have a powerful cocktail that would suggest China is about to devalue, and you need to be short CNY, and long treasuries. However, there is another way to look at this. China as an industrial goods exporter competes directly with Japan and Germany more than with the US. When we look at cross rates (ie CNY in Euro and Yen terms) we see no weakness in Chinese Yuan at all, unlike in 2016, when we last feared Chinese Yuan devaluation.

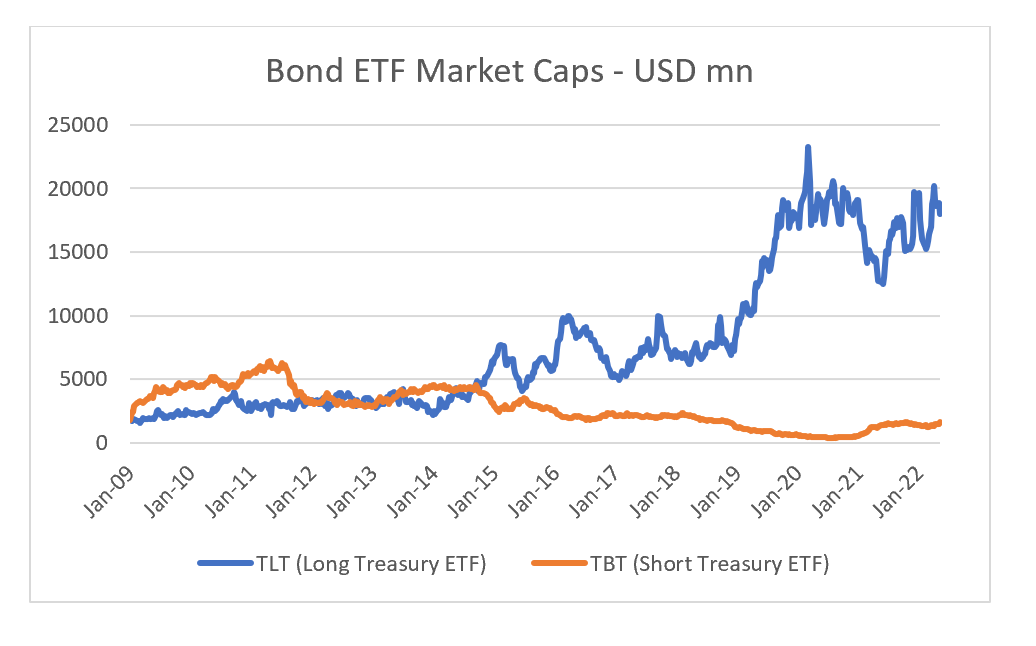

In the macro hedge fund world, it seems like the short treasury trade might be crowded, which would potential suggest a rally in bonds to clear out positions. However we can look at retail ETFs to get an idea of how money is really positioned. After the GFC, short bonds was also a popular trade, and the short treasury ETF has a market cap twice the size of the long bond ETF. Today the long bond ETF is 10 times the size of the short bond ETF. It would suggest to me positioning is still very light on the short bond trade.

Perhaps one way to square the weakness of the Asian dollar index is to try understand why the Euro and Yen are so weak? You don’t have to look very far. Commodities are soaring, and inflation is way above expectations, and both Japan and Europe have negative interest rates. Unless we start to see the Chinese Yuan weaken against the Euro and Yen, then inflationary bias will continue. Bonds still look bad news to me.