As I wrote about last month, I have tried to update my investment process to 4Ms - Motivation, Macro, Micro and Market. I then add a post called “Inflation or Deflation - A Trader’s Guide”. Implicitly, these two posts were related. Here I am going to explicitly bring them together. First things to talk about is Motivation. When I say motivation, I mean politics. And this is a new part of the process. At the moment it is driven by the question - Why does China refuse to devalue? In my investing career, every other country that has faced the Chinese combination of slowing growth, excess credit, and high land prices has chosen to devalue.

Since 2015, when Chinese exchange rate in real terms looked very expensive, it has remained so. I have added in a the the Chinese Yuan/USD exchange rate from 1981, and the BIS real effective exchange rate from 1994. My guess on Chinese “motivation”, is that they see no benefit in devaluing, as it would just engender a cycle of other currency devaluations. Also keeping their currency strong should promote domestic consumption and technological innovation. I find this easy to understand. If devaluation was a successful policy, Italy would be the richest nation in Europe, not Switzerland.

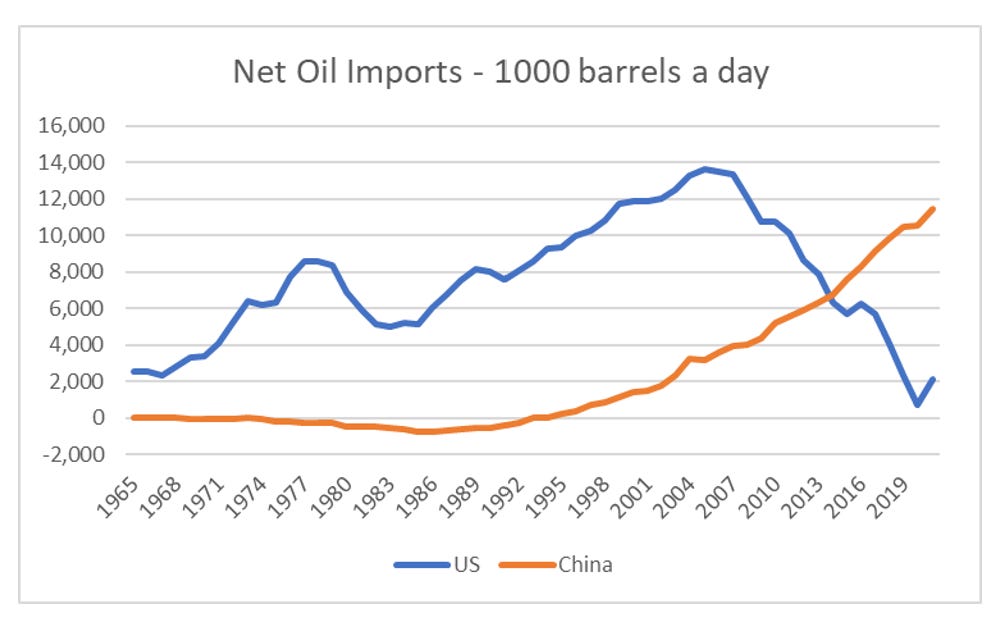

If this is Chinese policy (Motivation), then this makes China an “inflationary” anchor. Hence the 2nd M - Macro is that inflation and commodity prices should keep surprising to the upside. Why? Commodities should rise with Chinese wages. And China is now the price setter for the oil market.

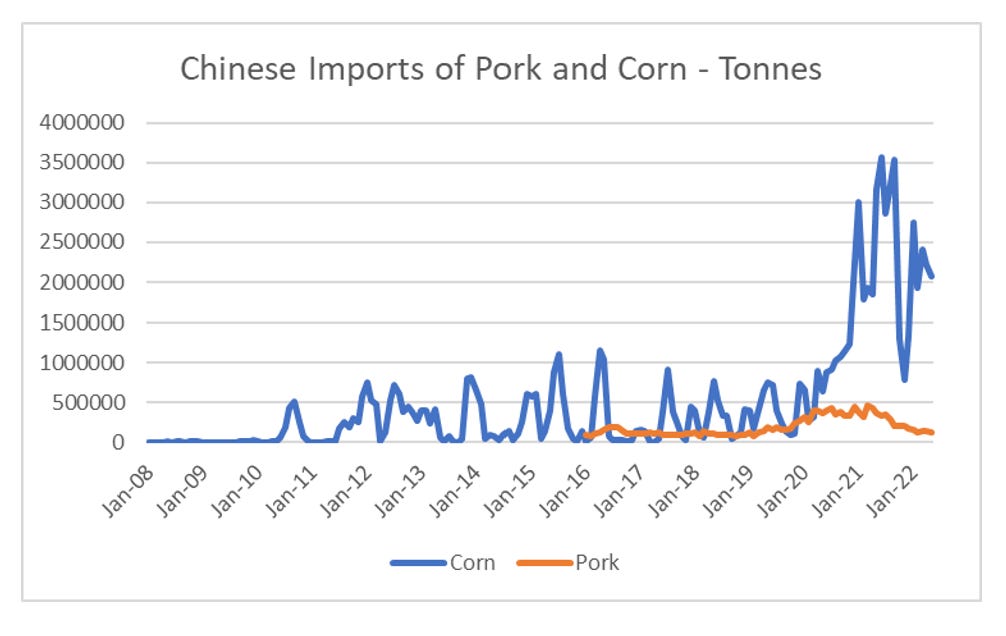

China is also the dominant importer of “food”.

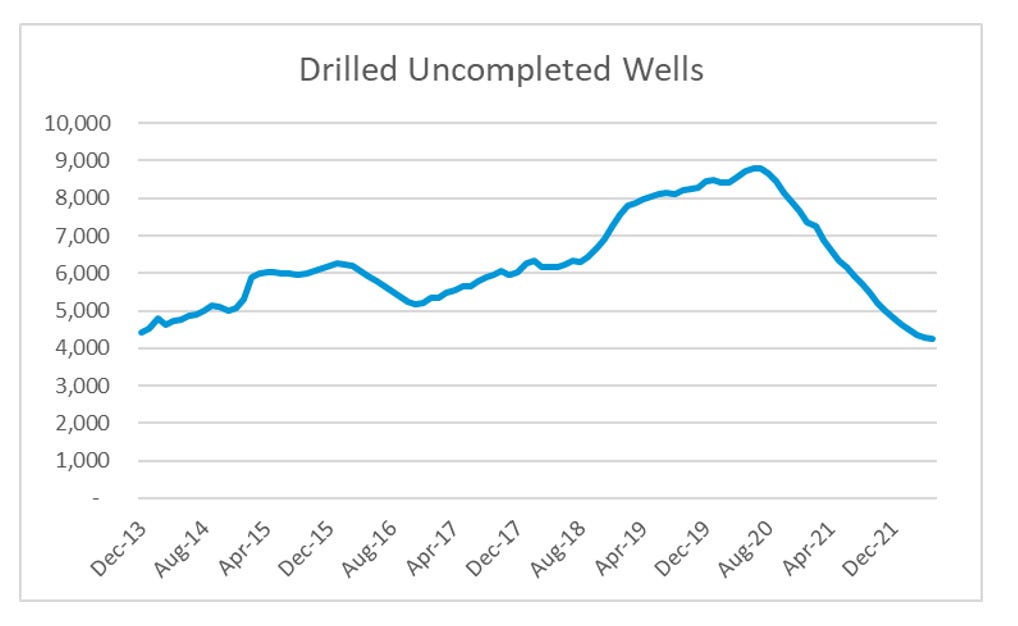

So the first two Ms - Motivation and Macro point to inflation. And they are showing a change that has been building over the past 5 to 6 years. So now we need to look at the third M - Micro. What are firms doing? One big change, particularly in the commodity area is that US oil firms (the shale producers are the swing producers these days) have run down their inventory of wells. This makes boosting production difficult.

Oil is an important, but not the only area that needs to be looked at, but for our purposes it is sufficient. So for me the first three Ms still point to inflation (Or a political system that favours labour over capital). What about the 4th M - Market. My preferred market indicator was a ratio of long gold, short treasuries in this environment.